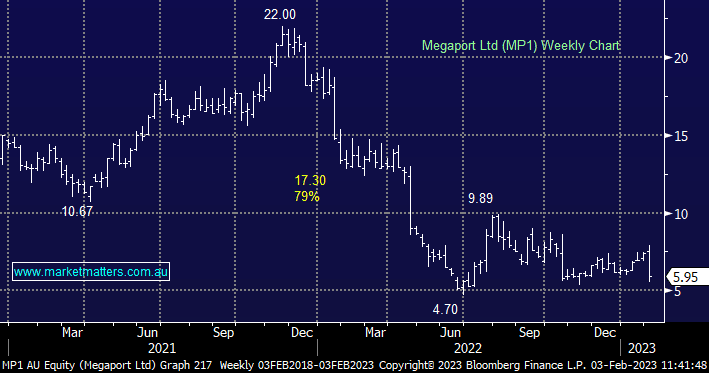

Hi Peter,

As you rightly point out, MP1 was whacked following a disappointing result, the crux of the issue stems from slowing growth with the number of ports being added simply not enough to justify its $1bn market capitalisation. We were also surprised that they burnt so much cash and have had to take on a credit facility that have earnings hurdles embedded in it, which is not a sign that MP1 is coming from a position of balance sheet strength.

We like the story of MP1, but its just simply too expensive for what they are delivering – there are not many companies trading on ~9x revenue anymore!

- MP1 is in the too hard basket for MM, we would rather pay a higher price once clarity is evident towards its future. The 9% short interest in the stock aligns with this view while we think they may need to raise equity at some point (hence investment banks will continue to push a more positive thesis on the stock than perhaps is justified!)

From a momentum perspective a break of its $4.70 low last year wouldn’t surprise. For a more positive take the