Thoughts please on Hotel Property Investments (HPI) & its property exposure

Hi MM Team, Could I please get your perspective on HPI and its real estate exposure? thanks Alain

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

Hi MM Team, Could I please get your perspective on HPI and its real estate exposure? thanks Alain

Hi Alain,

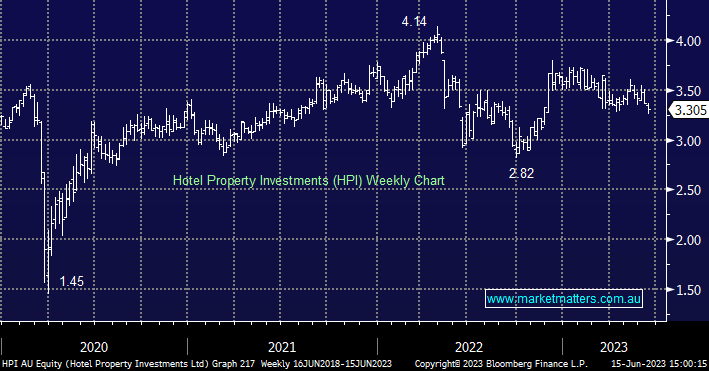

HPI own a suite of pubs across Australia, worth $4.06/sh as at 31 December. Valuations were revised 3.3% lower at the half year result, however shares are currently priced at an ~18% discount to NTA.

Recent transactions suggest an increase to the cap rate which would lower valuations for example HPI bought a Queensland pub on an initial yield of 6.2%, around 1.5% above the yield on NTA suggesting valuations have further to fall. The current discount to NTA is reasonably appealing and the stock is on a ~5.5% yield. Demand for quality hotel real estate remains strong and the company is geared at the lower end of the target range, a positive as interest rates climb.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.