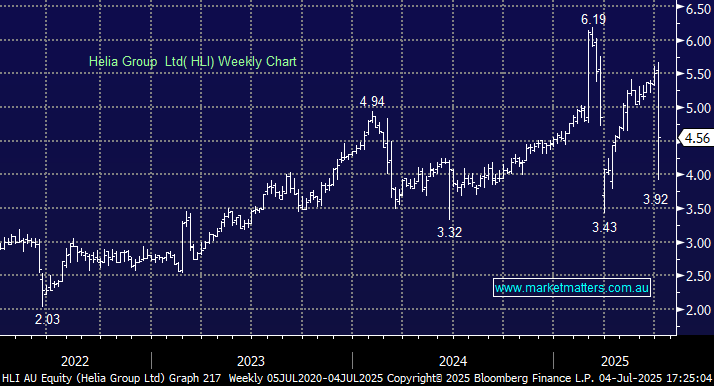

Hi Young,

It’s a good question. This has been a stock we’ve covered quite a few times over the years, and the rationale for buying it (with a small 2.5% initial weighting) is for income, derived from excess capital on their balance sheet. We will likely add to the position after we hear more from the company about further planned initiatives around capital management.

Our view currently, is that HLI is clearly not ‘going affter’ these contracts, and are more content to see business leave than write less commercial agreements. The likely loss of the ING contract this week, as with the loss of the CBA contract in March, will reduce earnings, however, it will also free up capital for agressive share-buy backs and higher distributions/special dividends moving forward. In our view, they will likely be able to offsett the majority of these losses on an earnings per share (EPS) basis by agressively buying back stock.

Their back book will also keep generating earnings from both CBA and ING for several years to come, and with ~$1.7bn of capital on their balance sheet, well in excess of the required $837mn (and falling), there is a lot of room to move here. Of this, around 60% is tied up with CBA and ING contracts hence the strong case for more payouts as these contracts roll off – the market cap of HLI is only $1.24bn.

- We are expecting a yield in FY25 (december year end) and FY26 of ~15% fully franked.