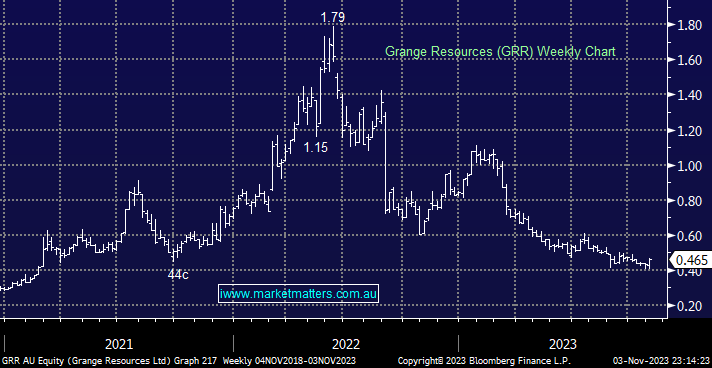

Why is Grange Resources (GRR) cheap?

Why is the P/E ratio of GRR lower then other iron ore companies like CIA, RIO and FMG?

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

Why is the P/E ratio of GRR lower then other iron ore companies like CIA, RIO and FMG?

Hi Giles,

Firstly lets look at the standout numbers that matter:

Its the been the same story across equity markets both home and abroad, i.e. the small caps remain unloved with investors opting for the saver “Big Caps” which have more established operations doing bigger volumes, which is very important in Iron Ore mining, volumes improve unit economics which improve earnings etc. GRR is a lower volume (higher quality) operation but we think bulk mining is more a scale business, and it’s simply hard to compete the big guys. As can be seen above GRR is the baby compared to the other 3 companies you mentioned.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.