Hi Alex,

The only positive to the result was subscriber growth in their streaming business ~30% above consensus which implies their target for achieving streaming profitability in fiscal 2024 should become reality. Still, the rest of the result was weaker than hoped with theme park margins softer and their broader direct to consumer (DTC) business which includes global advertising sales, overseas media assets, streaming and syndicated TV missing earnings expectations.

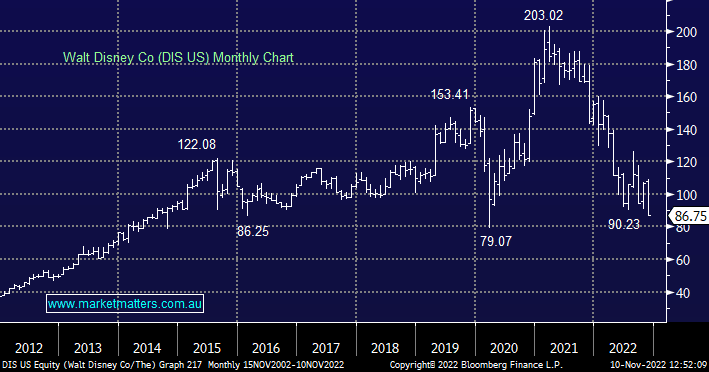

Clearly this is a big company that is being impacted by the broader macro environment leading to a ~5% revenue miss and more at the earnings line, however we continue to believe that Disney (DIS US) is best positioned to win in streaming supported by the best depth of content. We are holding our position.