Hi Bernie,

CCP (Credit Corp) has a simple business model, it makes money by buying bad debts cheaply, then collecting more cash from borrowers over time than it paid for the portfolio.

On the surface the financial metrics you mentioned do look attractive, revenue is forecast to grow ~17% from FY25 to ~$636mn in 2027, its trading well below its long-term valuation, while the stock is still forecast to yield 5.75% fully franked.

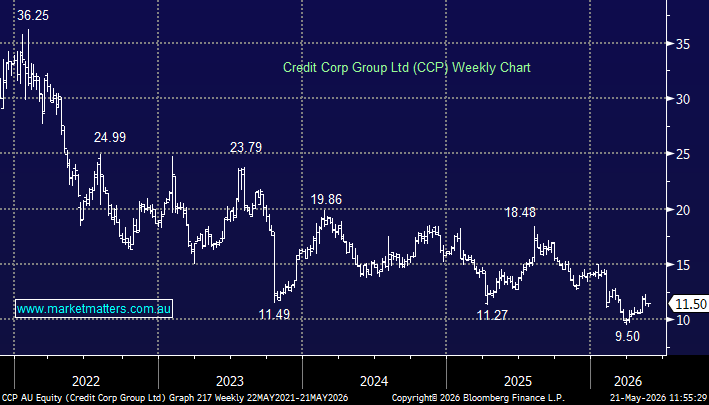

- Hence, the obvious question is why is Credit Corp trading near is 5-year low?

The real issue has been a drought in Australian and New Zealand debt supply. CCP’s core Australia/NZ debt buying revenue fell 6% to $108.1 million in H1 FY26 as post-COVID household savings buffers and benign credit conditions meant the major banks generated fewer charge-offs than normal — starving the group of fresh portfolios to acquire. Because CCP’s model relies on buying distressed debt at scale (which is essentially their inventory), weaker purchasing volumes today typically translate into softer earnings 12–18 months later.

- If banks generate fewer defaults and charge-offs, there are fewer portfolios available for CCP to buy, which means weaker future collections (revenue).

The US is now the growth engine, but it hasn’t yet fully offset the ANZ weakness. Interest-bearing credit card balances grew 12% over the half year, early signs of increasing supply in the ANZ debt market. The banks starting to increase provisions for bad debts is another good sign for CCP.

CCP remains a classic late-cycle recovery play that simply hasn’t seen the cycle turn yet. The structural thesis, rising consumer stress eventually driving higher debt supply, still holds, but the recovery has been slower than expected and investor patience is starting to wear thin.

- From our own perspective, we’re not that keen to buy a business like this, that relies of debt collection tactics that apply pressure to often vulnerable parts of society, and given the weak trend and recently weak results, we’ll be giving this one a wide berth.