Hi Chris,

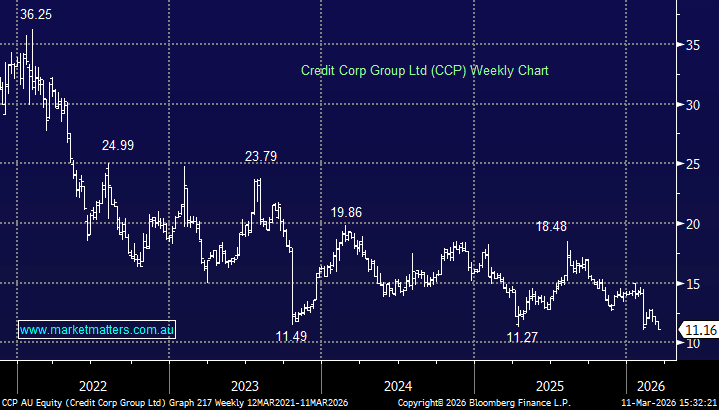

Debt collector CCP is trading near multi-year lows after being hammered well over 10% in early February following a disappointing 1H result:

- Revenue +4% YoY to $283.6mn.

- NPAT flat at $4.1mn.

- Dividend of 32c was unchanged.

CCP’s US business performed well, with revenue from its US debt buying segment rising 25% to $73.7m and NPAT jumping 63% to $11.7m. However, the group’s result was dragged down by weakness in Australia and New Zealand, where debt buying and collection revenue fell 6% to $108.1m and NPAT declined 10% to $10.9m after several issuers temporarily paused debt book sales, reducing collection volumes. The AU/NZ lending business delivered modest revenue growth (+4% to $101.8m) but NPAT fell 14% to $21.5m, despite a 14% lift in settled loans to $223.3m.

Also, CCP’s reduction in US purchasing guidance from $200-230mn to $160-180mn weighed on the stock with the best performing area likely to struggle moving forward.

Credit Corp performs best when credit growth is strong and banks are actively selling bad debt, while the economy remains stable enough for consumers to keep repaying. We agree it looks cheap ~$11, and yielding around 5.5% fully franked, but while the outlook for inventory (i.e. available debts to buy) is weak, we think they’ll remain challenged.