Hi Lindsay,

You’re right, the equation isn’t simple. Listed property vehicles like VAP are influenced by several competing forces – rental income, asset valuations and the cost of debt. While rents typically move higher over time and often keep pace with inflation, higher interest rates increase funding costs and push up the return investors demand from property (cap rates), which in turn tends to pressure asset valuations.

When assessing whether this is already reflected in prices, we typically look at cap rates and how REITs are trading relative to their Net Tangible Assets (NTA). Listed property often adjusts faster than the underlying physical market, so when REITs trade at a large discount to NTA, the market is usually pricing in either higher cap rates or further valuation pressure. We also pay close attention to balance sheets – particularly gearing levels, interest cover and debt maturity profiles, and how they employ hedging on this debt – because higher leverage means greater sensitivity to rising borrowing costs.

In simple terms, the key indicators are cap rate expansion, the size of any discount/premium to NTA and the strength of the balance sheet. If cap rates have moved higher and REITs are trading below NTA, the market has likely already priced in a fair degree of the higher-rate headwind, though the impact varies depending on leverage and specific area within property space.

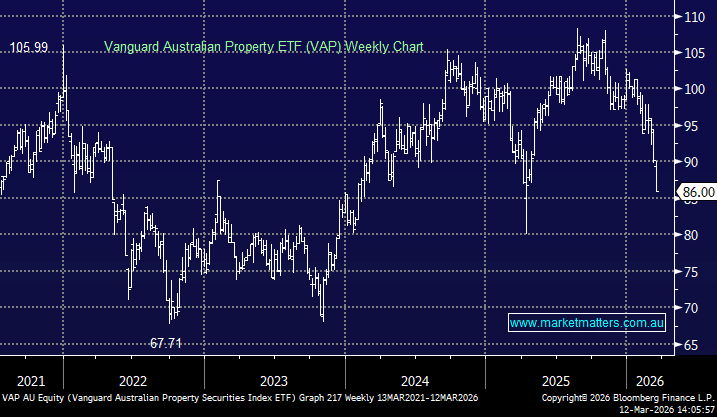

NB The VAP ETF is heavily weighted toward Goodman Group (GMG) ~36% which adds a significant tech influence on the mix, ever since GMG branched out into Data Centres, and has largely followed the value compression of the high growth/software stocks over the last 6-9 months, hence we prefer single stocks such as Mirvac (MGR), Stockland (SCG), Abacus Storage King (ABK) or Dexus (DXS) for a mix of real estate exposure, with all of these names, in our view, already pricing in materially higher interest rates.

Also worth remembering that bond markets often get ahead of themselves. The yield on the Aussie 10-year is now ~5%. Property stocks are pricing in this rate currently, but if higher oil prices start to impact growth, yields will start to come down. Yields and oil prices don’t typically rise as one for long.

This week we faded higher bond yields, by buying Mirvac (MGR) – a diversified operator within the property sector, growing earnings at mid single digits, with a 5.5% dividend yield, trading more than one standard deviation below it’s usual valuation, and at a 20% discount to their last reported NTA of $2.30. Mirvav hedges around 50% of it’s interest rate risk, which is lower than some of their peers like GPT, but that will provide MGR will more upside as/when bond yields come down – which is our core view. History tells us that quality diversified REITs often trade ±10–20% around NTA depending on the interest-rate cycle – clearly we’re at the bottom end of that range.