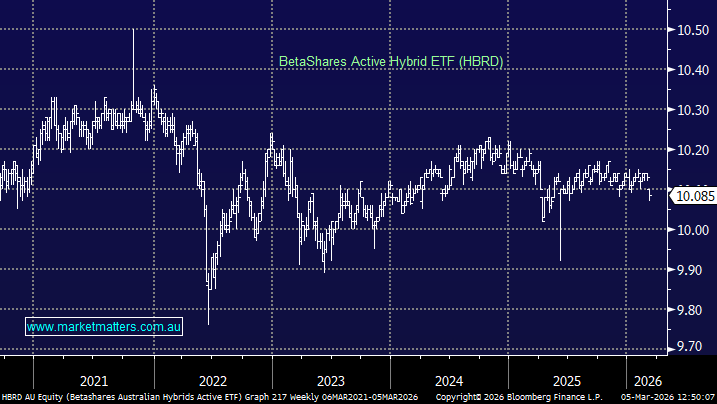

Hi Murray,

The changes to HBRD are fairly significant and reflect a structural shift in the hybrids market rather than just a minor ETF tweak. However, the changes are more about adapting to the end of bank hybrids than anything negative about the ETF itself.

The main driver of the changes is that APRA has decided to phase out bank hybrid securities by 2032, meaning banks will stop issuing new hybrids and existing ones will gradually be redeemed. This significantly reduces the investable universe for funds like HBRD, which is why the ETF is moving toward a broader credit strategy rather than pure bank hybrids, and will likely hold a higher proportion of tier 2 bank bonds, which is an area we like.

Overall, the ETF is evolving from a pure hybrid income fund into a broader credit income strategy, and we think this is a sensible evolution of the product under the circumstances.

- We own HBRD in the Core ETF Portfolio, and these changes do not change our positive view of the product.