Hi Andrew,

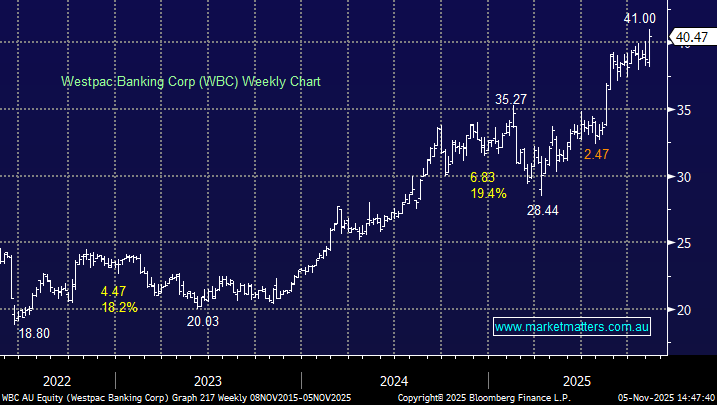

Local analysts have been pretty anti the banks for most of 2025 with valuation grounds their primary concern. On the MM website you can see 1 Strong Sell, 5 Sells, and 6 Holds on WBC with no Buys of any degree!

- The consensus price target (PT) for WBC is $34.06 and analysts underlying view a sell.

However, importantly the analysts have been wrong for most of 2025 and MM has no intention of following the pack by taking profit at this stage. WBC is up over +25% year-to-date with a second fully franked dividend due shortly, a great performance compared to the ASX200 which has advanced by less than 8%.

- We continue to like WBC as they deliver solid loan growth plus the markets looking for significant costs savings and efficiencies for the banks from the adoption of AI over the years ahead.

The path of least resistance remains up with the crowd looking/feeling underweight both ANZ and WBC and although they may consolidate recent gains once they trade ex-dividend this month, there’s no obvious reason to abandon banks just because think they are overvalued.