QBE leads the charge again (SBM, FMG)

WHAT MATTERED TODAY

A second day of gains for the ASX with the market trading back up above 6050 following on from the positive gains yesterday. Healthcare has a good day led by strong follow up buying in Resmed while QBE was in the spotlight adding another 5.37% to trade back up around $11.

The S&P/ASX 200 index rose 17 points, or 0.3 per cent, to 6054, while the All Ordinaries climbed 18 points, or 0.3 per cent, to 6168. The Australian dollar reached US80.13.

S&P/ASX 200 Intra-Day Chart

S&P/ASX 200 Daily Chart

CATCHING OUR EYE

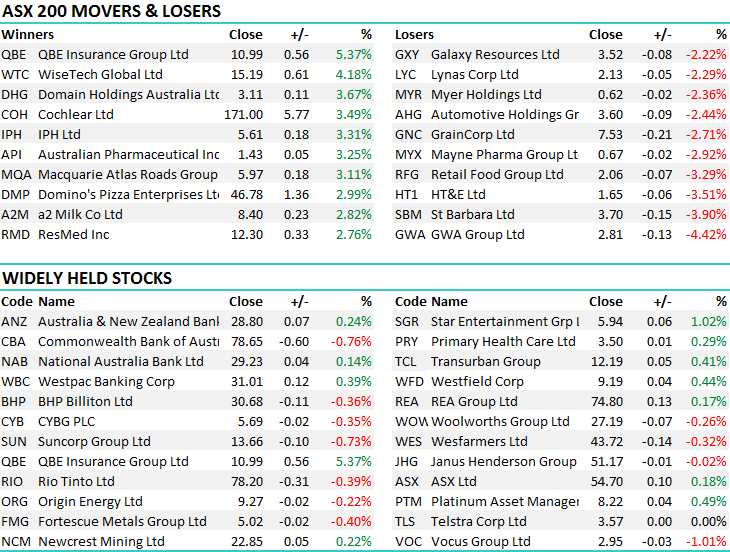

1. QBE Insurance (QBE) $10.99 / +5.37%; QBE was the most improved in the top 200 today, now seemingly a far cry from the downgrade announced yesterday. Since it’s 10:11AM low yesterday of $9.86, QBE has risen a huge $1.13 / 11.5%. Today’s jump came despite 4 brokerage houses cutting their price target, however although Macquarie reduced their price target, they upgraded their outlook to outperform – which is BUY. They reckon that within QBE, there are 5 key portfolio’s that QBE should look to divest in order to simplify the business; Australia Personal, LMI, Argentina, Latin America & Asia.

Although there is a long road ahead, it seems that after years of disappointing investors the market was anticipating a much bleaker outlook from the company, but instead received some tentative signs that the worst is over. The price action over the last few days goes to show how negative the market was towards the stock, positioned against it and are now forced buyers. We hold QBE in the Growth Portfolio.

QBE Insurance (QBE) Daily Chart

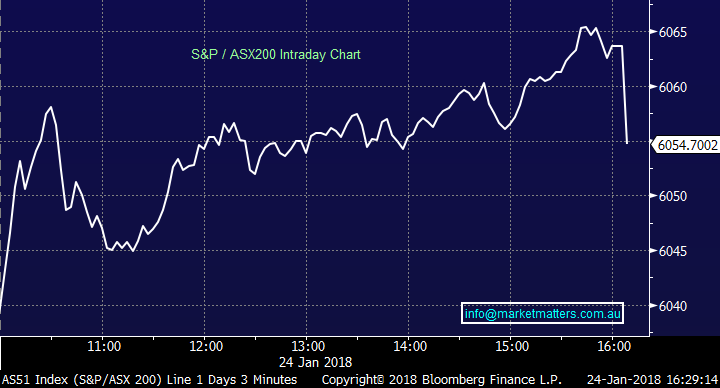

2. St Barbara (SBM) $3.70 / -3.9%; SBM appears to have run too far for its own good recently, with target prices upgraded but performance outlook downgraded. The gold miner and explorer had a stellar end to 2017 after delivering strong cash flow outcomes in August whilst ramping up production in the back end of the year. Jumping nearly 50% from October lows, analysts deemed that the run had gone too far, and doubted whether the strong numbers could continue. We have gold exposure through NCM.

St Barbara (SBM) Daily Chart

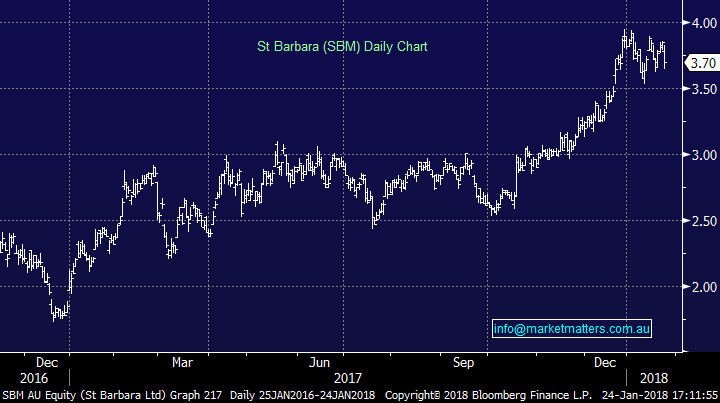

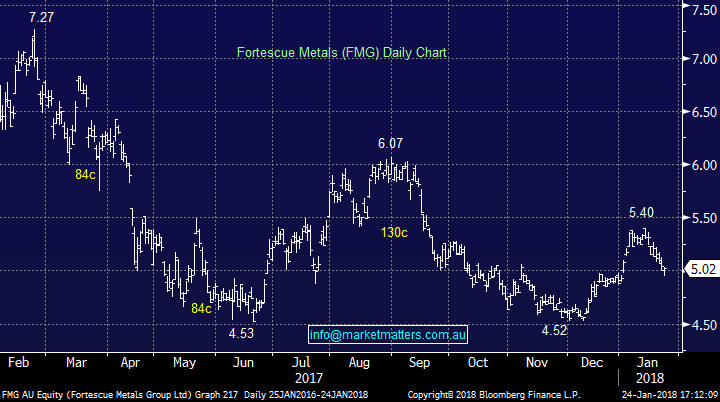

3. Fortescue (FMG) $5.02 / -0.4%; FMG fell alongside Iron Ore futures in Asian trade today. Iron Ore has taken a hit in the last few days after Barclay’s and ING warned that profitability of Chinese steel mills has been squeezed and will lead to lower demand and prices for Iron ore. In our view, the banks have jumped the gun here and iron price gains have really lagged the increase in steel prices being received by mills, as shown in the chart below.

Iron Ore Futurers (WHITE) vs Steel Index (ORANGE) Daily Chart

We used this dip to enter FMG today in the Income Portfolio.

Fortescue (FMG) Daily Chart

OUR CALLS

We added FMG to the Income Portfolio today below $5

Z1P order remains open at $0.84, closing today at $0.965 – however we concede the ship has probably sailed here.

Have a great night

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 24/01/2018. 5.00PM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here