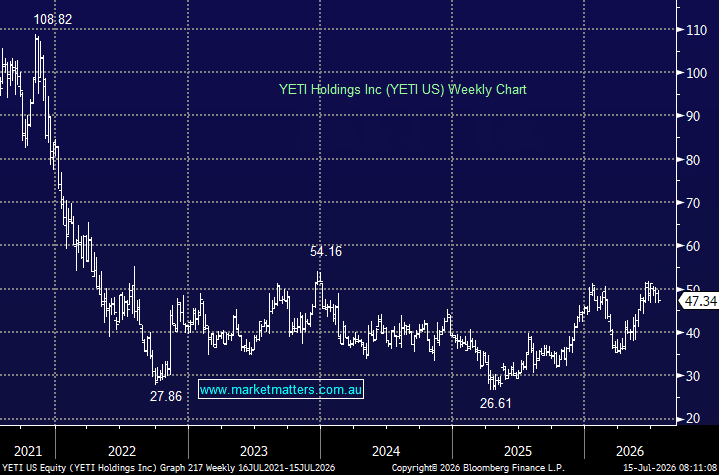

YETI has now reached our initial target and is trading near the top of its recent range following a strong recovery in the share price. We continue to like the business and remain comfortable holding it in the International Equities Portfolio, although the position now warrants a more disciplined approach after the gains already delivered.

The valuation is not demanding. YETI is trading on around 15.5x forward earnings, modestly below its five-year average of approximately 17x, with earnings expected to grow by around 8–9% annually over the next few years. Consensus forecasts point to adjusted EPS rising from US$2.88 in FY26 to US$3.31 in FY27 and US$3.65 in FY28, supported by continued revenue growth, improving operating leverage and a strengthening balance sheet.

The company’s fundamentals remain sound. Its premium brand continues to resonate across drinkware, coolers and outdoor equipment, while wholesale momentum has been particularly encouraging. The strong wholesale performance reported in 1Q suggested retailers were rebuilding inventory, allocating more shelf space to new products and responding positively to consumer demand. We’ll get another update on these dynamics on their 2Q results due on the 7th August.

YETI is also producing strong cash flow. Free cash flow is forecast to remain around US$200–280m annually, while the balance sheet is expected to move further into a net cash position. This provides flexibility for continued investment, product development and share buybacks, including the recently expanded US$500m repurchase program.

There are still risks to monitor. YETI is exposed to the health of the US consumer, its products sit firmly in the premium discretionary category, and tariffs remain a potential headwind for gross margins. Direct-to-consumer sales were also softer than wholesale in the last result, which leaves some uncertainty around underlying end-demand if retail restocking fades.

We still regard YETI as a hold. The business remains high quality, cash generation is strong and the valuation is reasonable, but with the stock now at our initial target and near the top of its recent trading range, the near-term risk-reward is less compelling than it was. After a year in which returns across the International Equities Portfolio were too polarised and heavily skewed to the 1H, we are increasingly conscious of locking in gains when opportunities arise. We are not rushing to exit just yet, but the position is on close watch.

MM remains cautiously bullish YETI ~$US47

Add To Hit List