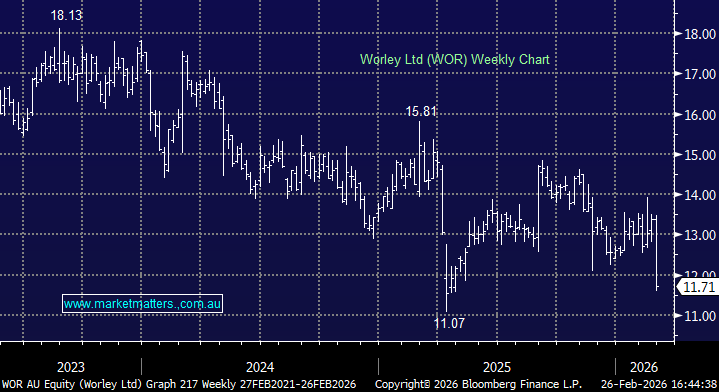

WOR -10.2%: Was eventually hit hard after a 1H result that was ahead of consensus at the EBITDA line, but raised fresh concerns around the quality of earnings and the outlook for FY26 growth. Shares opened higher but fell away as the day progressed.

While underlying earnings of $377m was marginally higher year-on-year and ahead of consensus, the result was clouded by significant restructuring costs below the line, which distorted comparability versus consensus expectations. Statutory NPAT fell 35% to $119m, well below market forecasts, reinforcing investor caution despite management reiterating guidance.

1H26 Highlights

- Underlying EBITA $377m, +0.3% y/y – beat consensus

- Underlying NPATA $207m, down 4.2% y/y

- Statutory NPAT $119m, -35% y/y, well below consensus

- Aggregated revenue $6.31bn, +5.4% y/y, ahead of expectations

- Interim dividend held at 25c

- Backlog solid at $16.7bn, with continued major project wins

- FY26 margin guidance (ex-procurement) reiterated at 9.0–9.5%

This was a messy result because it relied on adjustments that make underlying growth appear weaker than previously expected. While Worley reaffirmed its FY26 outlook, commentary suggested like-for-like growth may undershoot earlier assumptions. On the positive side, the strategic direction is unchanged. Management continues to simplify the business, targeting more than $100m in annualised cost savings from FY27, while exposure to energy transition, resources and infrastructure remains a structural tailwind. WOR also intends to extend its on-market buyback of up to $500m.

However, with restructuring still weighing on statutory earnings and growth expectations now under scrutiny, the market has opted to sell first and ask questions later.

MM is now reconsidering our position in WOR

Add To Hit List