- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

With China off on Golden Week holiday, there was a void of any positive policy news from the region and with the start of a new quarter, it wasn’t surprising to see some weakness creep into the market, the index giving back the gain it put on yesterday with both the miners & banks attracting sellers.

- The ASX 200 fell 60pts/-0.74% closing at 8208

- Healthcare (+1.12%), Utilities (+0.92%) and Communication Services (+0.72%) were solid

- Materials (-2.29%), Financials (-1.19%) and Industrials (-0.57%) were the drags.

- Retail sales came in hotter than expected today, printing 0.7% for August vs 0.4% expected and removes some pressure on the RBA to cut rates this side of Christmas, all that could change with the next print!

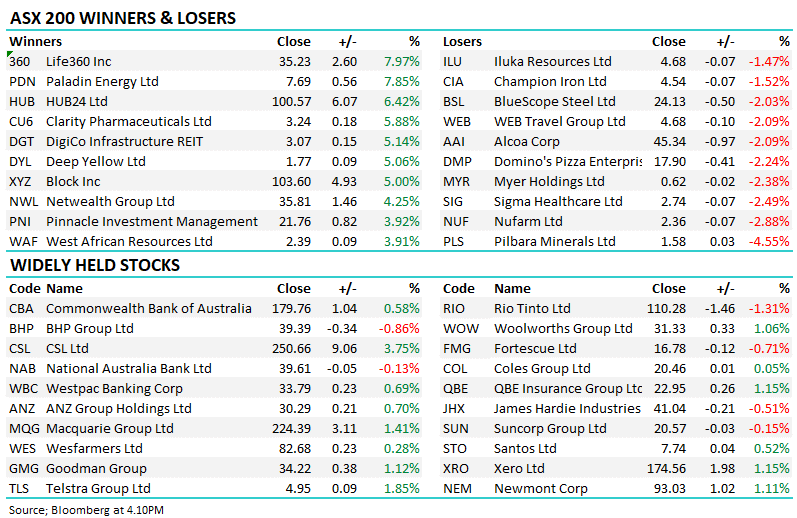

- REA Group (REA) +4.9% rallied after pulling its bid for UK listed Rightmove following 4 bids with little engagement from the target.

- Shares in Rightmove were down ~7% overnight, though they’re still ~11% higher than they were pre-bid. REA may be back at some point next year, but a good call we think to walk away for now.

- Sigma Pharma (SIG) +22% rallied after the ACCC seems to be engaging with their proposals to address the main sticking point of them acquiring Chemist Warehouse, being the confidential data on competitors the merged group will have access to.

- SIG/CW are promising to play nice with a range of undertakings that the ACCC is now seeking views on.

- Qantas (QAN) -3.37% fell after Qatar Airways moved to buy 25% of Virgin Australia.

- Resmed (RMD) +1.54% said it can deliver high single-digit revenue growth over the next 5 years, as it launches new products designed to treat insomnia.

- Fortescue (FMG) -3.45% led the other miners lower, BHP Group (BHP) -2.87% & Rio Tinto (RIO) -2.63%.

- Commonwealth Bank (CBA) -1.51% & Westpac (WBC) -1.67% were the weakest of the banks, while National Australia Bank (NAB) -0.59% fell the least on further cost cutting.

- No trade in Iron Ore with December Futures sitting at $108/MT ahead of the holiday.

- Gold was weaker overnight before rallying ~$US10 during our time zone today, sitting $US2645/oz, around our close.

- China & Hong Kong were closed, the Nikkei in Japan was up over 2%.

- US Futures are flat.