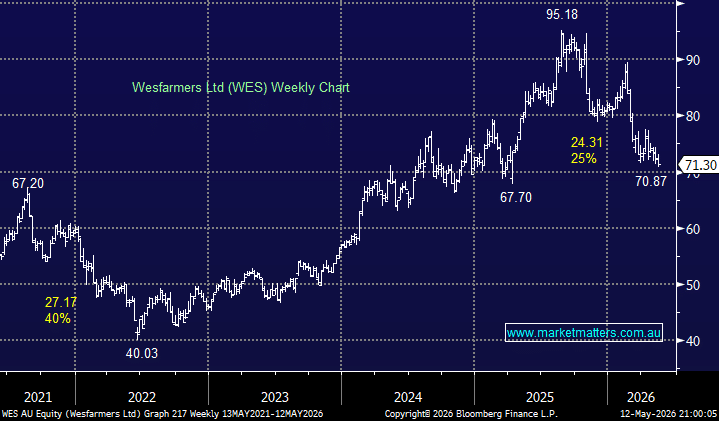

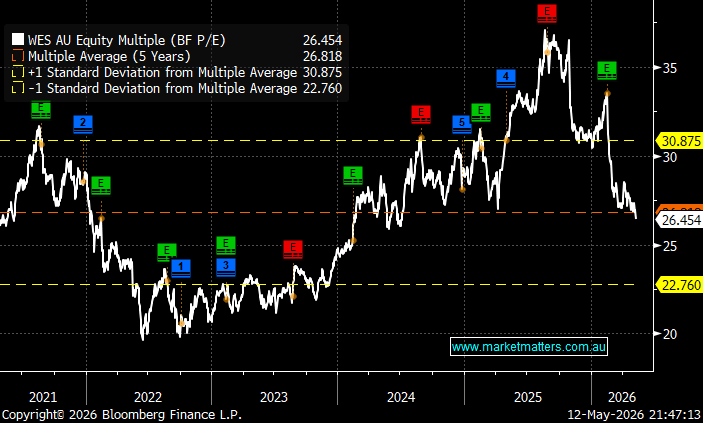

Wesfarmers was a dominant member of the “Certainty Trade” which propelled several high flying “Blue Chips” to unprecedented levels (and valuations) in 2025. However, as we’ve also seen with the likes of Commonwealth Bank (ASX: CBA) and JB Hi-Fi (ASX: JBH) momentum buying is not enough to hold stocks at expensive valuations when the economic backdrop deteriorates, in fact it can often lead to subsequent underperformance. However, after correcting 25% from last year’s high, Wesfarmers is only trading back around its average valuation of the last 5-years, aided in part by its sustainable 3% fully franked yield and “defensive” nature.

Australia’s most diversified retail and industrial conglomerate, owns Bunnings, Kmart, Target, Officeworks, Priceline, and a growing chemicals, fertilisers and mining divisions, making it one of the few ASX companies capable of generating earnings growth regardless of which part of the economic cycle is dominant, hence it carries the defensive tag at times, especially compared to many of its retail peers. The numbers through 2026 reflect how the stock is treated when investors expect the Australian consumer to come under pressure, no surprise, with the RBA having already delivered three rate hikes this year and further tightening likely:

- Year-to-date: Temple & Webster (ASX: TPW) -61%, Nick Scali (ASX: NCK) -39%, Harvey Norman (ASX: HVN) -37%, Super Retail Group (ASX: SUL) -30%, JB Hi-Fi (ASX: JBH) -27%, and Wesfarmers (ASX: WES) -12%.

Wesfarmers delivered a solid 1H26 result with net profit after tax growing +9.3%, primarily due to a materially stronger-than-expected performance from its chemicals and fertilisers division. They also upgraded lithium guidance from a full-year loss to second-half profitability as spodumene prices strengthened. However, the retail businesses were softer across the board, for a number of reasons, overall reflecting a cautious consumer.

- Bunnings (~43%) and Kmart (~25%) dominate revenue both now and forecasted in the years ahead making this them the critical operations which will drive Wesfarmers share price.

However, the stock received an encouraging read through from Metcash’s (ASX: MTS) result this week, covered Here, which saw MTS rally more than +6% on the day helped by improved sales momentum in tools and hardware during the second half. This was an encouraging net read-through for Bunnings’. If independents are maintaining share in trade, it suggests underlying activity in residential construction is holding up enough to support volumes. However, Management also flagged that the residential building environment has deteriorated versus the “green shoots” seen in mid-2025, pushing out the expected recovery. In MM terms, the cycle remains intact but delayed – volumes are holding, but margin pressure persists and any meaningful commercial uplift is now a medium-term story rather than imminent.

The WES share price shrugged off the MTS result, making new 12-month lows yesterday conveying the message that there’s no urgency to buy the stock/sector in the current environment. Wesfarmers is an exceptional business with genuinely resilient earnings and compelling long-term growth optionality, but the problem is the price, it’s not cheap unlike many other retailers, a two-edged sword as it reflects quality but capped valuation expansion when the worm eventually turns in favour of retail.

- We can see long-term value emerging in Wesfarmers below $70 and have added it to our “Hitlist.”