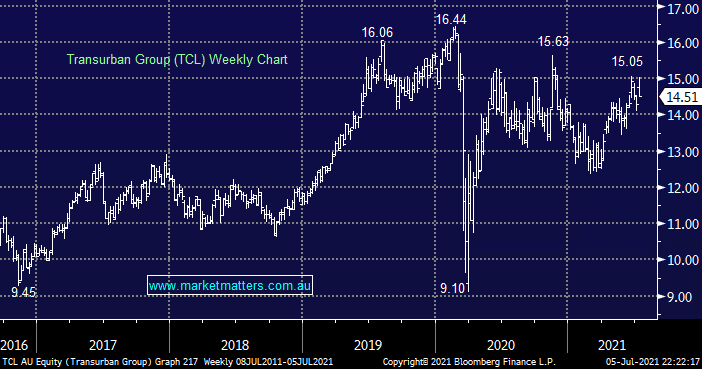

Toll road operator TCL has understandably struggled through COVID as the traffic on our roads has fallen, dramatically at times as lockdowns continue to roll across the country. This is a solid business although rising bond yields are likely to create periods of underperformance, we can see suitors liking this $40bn business but from a risk / reward perspective our preferred entry is ~$13.50.

MM is bullish TCL medium term

Add To Hit List

NB We hold TCL in our Active Income Portfolio: Click here to view