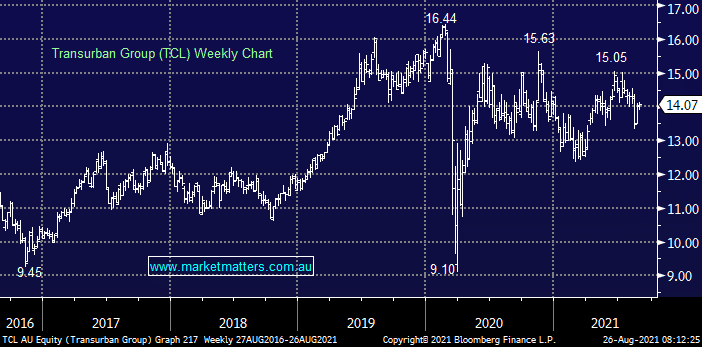

MM has been holding TCL in our Income Portfolio for well over 12-months and its currently showing us a nice paper profit but as the economy reopens and people get back in their cars this toll operator will make more money and theoretically pay more dividends hence TCL remains a yield play MM likes for what will hopefully be the new norm in 2022 and beyond. There’s also the outside possibility that somebody might consider a play for TCL’s quality assets, while it’s a large $39bn business there is an unprecedented amount of money looking for a safe quality home.

MM is bullish TCL initially targeting $16

Add To Hit List