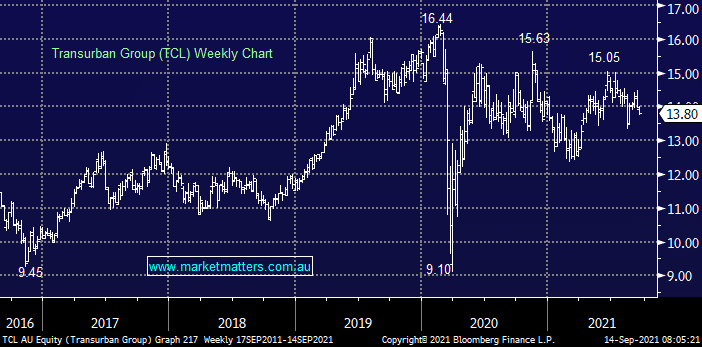

MM is holding TCL in our MM Income Portfolio, it has very similar rationale to SYD plus there are no foreign ownership caps which makes is an easier proposition for overseas suitors. Interestingly the TCL chart looks like a carbon copy of SYD before the takeover activity unfolded.

- TCL will benefit from the end to lockdowns as we all start using our cars again, assuming we can afford the petrol!

- MM likes TCL’s forecasted 3.3% yield over the next 12-months.

MM likes TCL below $14

Add To Hit List