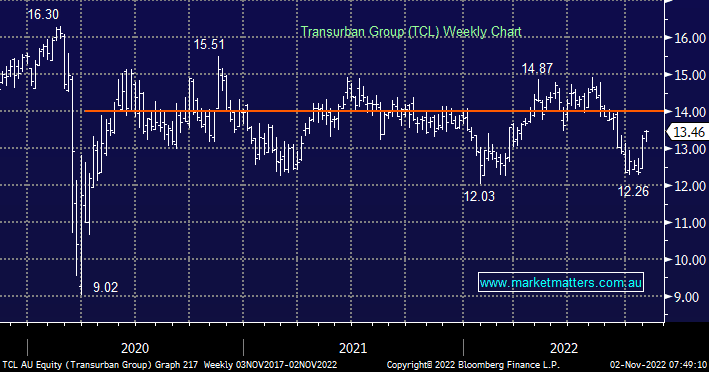

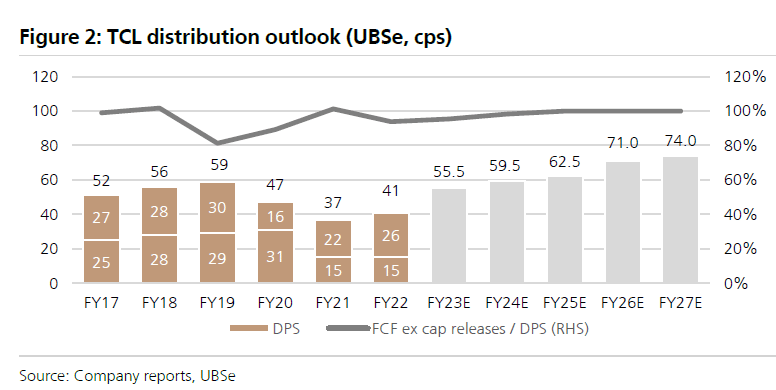

On face value, the toll road operator is a solid defensive stock, offering a reasonable ~4%, largely unfranked yield while their high levels of debt are seen as a risk in this sort of interest rate environment, however, there is more to this story which underpins our positive view on the stock. Growth in earnings and therefore dividends will be strong over the next 5 years with consensus growth rates of 8.5% from FY23-FY27 driven by new assets ramping up (WestConnex Stage 2 & North Connex) and continued recovery from covid impacted assets. This is also supported by revenue linked to CPI which as we all know is running hot along with expected capital releases which will also support dividend growth over the coming years – now more important with dividends derived from free cash flow + capital returns.

On UBS estimates, we have cycled the low point in yield from Transurban (TCL) and by FY24 the yield will be back up above pre-covid levels and will rise steadily from there.

chart

TCL distribution outlook – Source Company reports, UBSe

chart

TCL distribution outlook – Source Company reports, UBSe

For a defensive earnings stream backed by critical and irreplaceable infrastructure with a compound annual growth rate of ~8.5% over the next 5 years that actually benefits from inflation, it’s hard not to like Transurban (TCL), and this remains a core holding in our income portfolio.

MM remains bullish & long TCL in our Income Portfolio

Add To Hit List