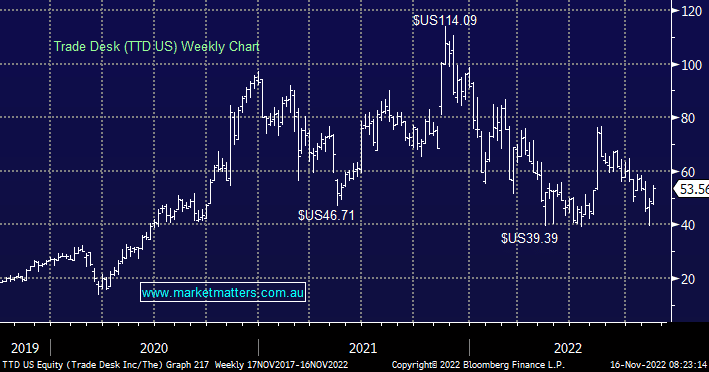

The advertising technology company reported quarterly earnings last week that defied some of the doom and gloom that we have seen elsewhere in digital advertising. While this is a volatile/high beta stock and shares have lived up to that reputation post results, the core metrics we like to track for TTD US continue to show a business moving in the right direction.

- Revenue growth for the quarter was +31%, while their guidance for Q4 for sales of at least $490m represents a 24% increase if they meet this number, TTD typically beat.

- Importantly, they are guiding to EBITDA of $229m for the quarter which is solid in a market that is meant to be struggling i.e. TTD is a rare bright spot showing resilience in a tough environment – a trait we like.

- Client retention has been stable at 95%, holding onto customers in a challenging period is a very good sign.

- They are profitable, have no debt plus they have $1.3bn in cash meaning they have no need to raise $$ at depressed levels.

MM remains long & bullish TTD US ~US$50

Add To Hit List