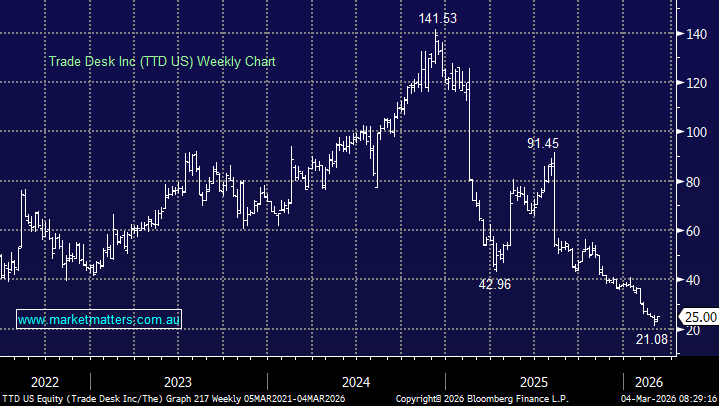

We own TTD in the International Equities Portfolio, and the journey over the past year has been frustrating, with the stock now off ~40% from our original purchase price. What was once a premium, high-conviction growth story has been steadily de-rated as growth slowed, competition intensified, and the macro backdrop turned less friendly for brand advertising.

- However, the latest result, and more importantly, the market’s reaction to it, suggests the stock may finally be starting to find a base.

For those not familiar, TTD is a leading independent demand-side platform (DSP), enabling advertisers to programmatically buy digital advertising across the open internet. Its AI-driven systems sort through millions of ad impressions per second to find the most efficient match for an advertiser’s objective, lowering cost-to-serve and improving targeting outcomes. It effectively sits at the centre of the digital advertising ecosystem.

They reported quarterly results at the end of last week, and while the 4Q25 was ahead of expectations, guidance for the 1Q26 was below. The stock initially fell, but is now recovering, implying to MM that the market has already adjusted to lower growth expectations, having sold the stock down aggressively from ~$US140 in 2025 to just $US25 today.

4Q25 Highlights

- Revenue: $847m (+14% YoY) vs $842m consensus

- Adjusted EBITDA: $400m vs $378m consensus

1Q26 Guidance

- Revenue: ≥ $678m vs $688m consensus

- Adjusted EBITDA: ~$195m vs $221m consensus

The quarter itself was solid. Revenue and EBITDA both beat expectations, and video, including Connected TV (CTV), now accounts for roughly half of the business. For FY25, revenue grew 18% to $2.9bn, slower than the 26% delivered in FY24 but still healthy in absolute terms.

The issue was guidance. Management flagged continued weakness in automotive and consumer packaged goods (CPG) , which together represent over a quarter of gross spend. Those categories are highly exposed to economic uncertainty (and tariffs), and brand budgets are typically the first to be cut when conditions tighten. The implied ~10% growth in 1Q26 is the slowest pace in around six years. Historically, that sort of guide would see the stock down heavily, but the reaction has been relatively muted.

TTD has already endured a significant de-rating, now trading on roughly ~6x 2027 EV/EBITDA estimates relative to its historical average of ~41x. Expectations had already been reset. When disappointing guidance fails to produce fresh capitulation, it often suggests a lot of bad news is already in the price.

There are still real risks for TTD. Competition from Amazon’s demand-side advertising platform (DSP) remains a headwind, particularly given Amazon’s data advantage and lower fees. AI is also lowering switching costs between platforms, which could pressure pricing over time. The deceleration in growth from 26% to 18% to potentially 10% near-term cannot be ignored. That said, management made an interesting comment on the earnings call: excluding auto and CPG, the business would have grown north of 20%, implying the core engine remains stronger than headline numbers suggest. In addition, spend commitments from its largest customers doubled during 2025, which should provide some underpinning to medium-term revenue.

Strategically, TTD continues to focus heavily on Connected TV through its Ventura ecosystem, an initiative aimed at creating a more transparent, content-agnostic operating system for CTV. It’s part of a broader attempt to counter the dominance of closed ecosystems and reinforce the “open internet” positioning that has always been central to our investment case.

We’re not calling an immediate rebound in growth. 2026 is likely to be a year of rebuilding confidence rather than reclaiming peak multiples. But with valuation reset, expectations lowered, and the stock no longer collapsing on soft guidance, the risk/reward is becoming more balanced. In MM’s view, TTD has moved from being priced for perfection to being priced for disappointment. If growth stabilises in the mid-teens and re-accelerates as cyclical headwinds ease, there is meaningful upside from here.

- For now, we remain holders, watching for evidence that the base that appears to be forming is real.

MM is cautiously bullish TTD US ~$US25

Add To Hit List