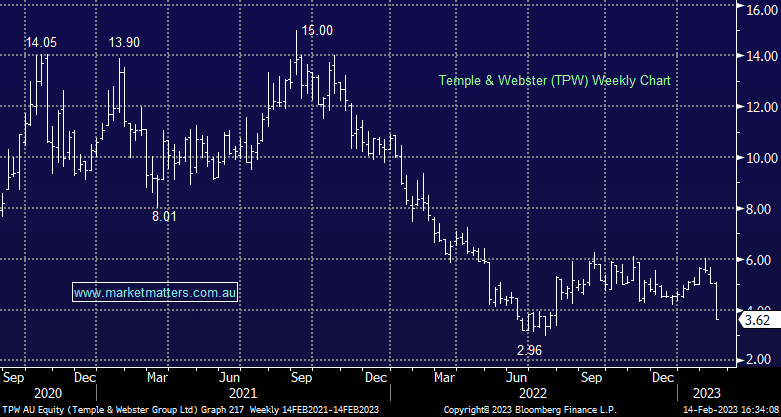

TPW -26.87%: the e-commerce furniture retailer struggled today following some sour comments at the half-year result. The numbers themselves were largely as expected with revenue of $207m just 2% below consensus while EBTIDA of $8.5m was a ~20% beat. Margins improved into the end of the year as the company benefitted from high supplier inventory and lighter-than-usual promotional offers. Supply chain costs were up, but less than expected and marketing expense margins fell substantially as the company cut costs. The concern came with forecast numbers where the company dropped the “double-digit growth” target over the medium term. Sales for the first 5-weeks of 2023 were down 7%, blamed on elevated comps as a result of the Omicron outbreak in January 2022. Their venture into an online Bunnings competitor is also chewing through cash faster than expected without the results coming through. Overall it seems e-commerce is struggling to keep up with the competition of bricks and mortar operations with an online presence.

MM is neutral TPW

Add To Hit List