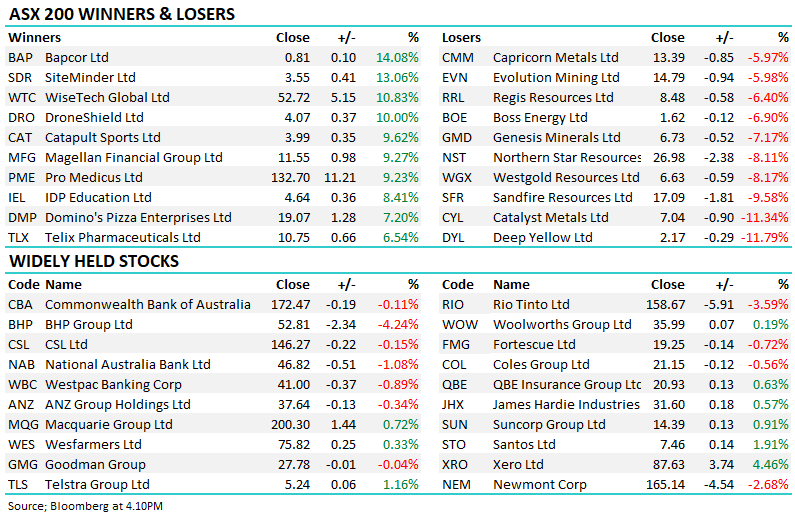

The mining and services contractor has fallen by -7.04% since the start of the month, though partially offset by a 2c fully franked dividend. The fall has come on the back of pressure on the value end of the market, but also attributed to a softer outlook for infrastructure which has weighed on the space with selling pressure on SRG compounded by what was perceived as a weak result by the market – we discussed the result here. In our view, the stock is cheap and we have no major concerns with their outlook, the market does not agree with this view for now!

SRG has a small exposure to Government work, making up ~10% of contracts won last year and we are yet to see any reason any of this work would be cancelled. These contracts tend to be at a lower margin compared to the ~20% EBITDA margins seen in Mining Services, so the revenue impact, if any, would have a less meaningful impact on earnings. The bulk of the exposure lies with major mining and construction firms who are well capitalized, i.e. projects that have little risk of being cancelled.

SRG ended the year with $1.9b of work in hand, up 46% for the year, with a further $6.5b of pipeline to bid on (up from $6b). It is trading on ~9x FY24 PE and guiding to 20% EBITDA growth which we see as conservative based on the pipeline of work available and the significant contract wins the company picked up last year. We are also expecting higher cash conversion this year after they brought forward some spending to FY23 to drive growth.

- MM will look to increase our 4% weighting in SRG into further weakness if it prevails.

MM remains long and bullish SRG

Add To Hit List