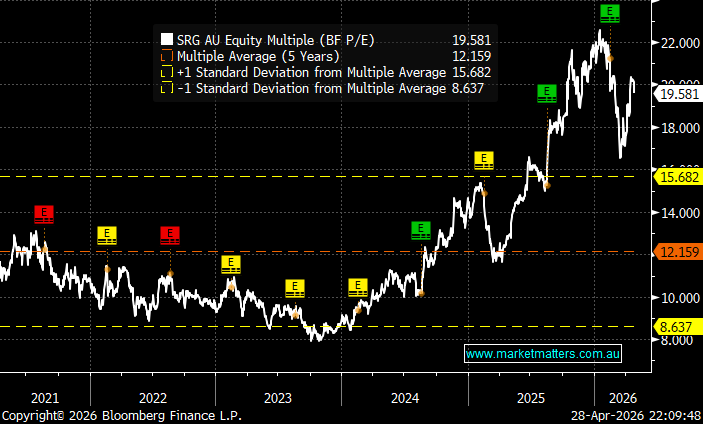

SRG Global entered the ASX200 in March after rallying +120% over the last year, taking its market cap to $1.8bn. The inclusion places SRG alongside established peers, including Downer EDI (ASX:DOW), Monadelphous (ASX:MND) and Worley (ASX:WOR), all of which operate across engineering, maintenance and infrastructure services. The company is certainly performing, with revenue on track to double in FY26 from the $809mn in FY23. However, the stock is priced for ongoing strong performance, with its current valuation significantly above its historical averages.

SRG’s re-rating is a textbook case of a quality industrial finally getting the recognition it deserved, driven by five key catalysts:

- Earnings: FY25 revenue was up 24%, profit up 52%, dividend up 20%, consistent beats in a market starved of genuine earnings growth.

- The Diona acquisition: In September 2024, the bolt-on acquisition of water and energy services business Diona was integrated successfully, adding recurring revenue in high-growth sectors.

- Recurring revenue model: Long-term maintenance and industrial contracts with blue-chip mining and infrastructure clients provide earnings visibility.

- Technology adoption: Drone-based inspection technology replacing manual labour on towers, bridges, and wind turbines is compressing costs and lifting margins.

- ASX 200 inclusion: Last month’s index promotion to the ASX200 forced passive fund buying and lifted institutional visibility, adding a structural demand tailwind to an already strong fundamental story.

SRG is a classic case of a boring business in the right place at the right time — maintenance, infrastructure, mining services, and energy transition exposure, wrapped in a recurring revenue model with impressive management. The re-rating from sub-$1 micro-cap to the ASX200 reflects genuine execution.

- The key risk from here: at a P/E of close to 20x, much of the good news is now in the price, and the stock has already shown it is capable of a correction, having retreated 26% from its January highs.

The next earnings print in August 2026 will be the critical test of whether the growth story has legs beyond the Diona integration tailwind.

SRG’s valuation is high for this type of business, which traditionally trade on a high single digit or low double digit multiple. Therefore, the company needs to continue to deliver growth to justify the current share price, leaving plenty of room for disappointment.

Conversely, Worley (ASX:WOR), which we own in our Active Growth Portfolio, is trading almost 30% below its 5-year average valuation, not helped by several broker downgrades this month after the company announced that it expects a $40mn hit to earnings due to the Middle East conflict, although it did say it still expects the underlying EBITDA margin to be within the 9-9.5% range, with no project cancellations so far. From a share price perspective, WOR initially dropped ~6% on the news but has encouragingly already regained most of the drop, with the transparent update likely to placate nervous investors.

- We can see SRG making new highs in 2026, but prefer Worley (WOR) through 2026 from a valuation perspective.

MM is neutral towards SRG around $3.00

Add To Hit List