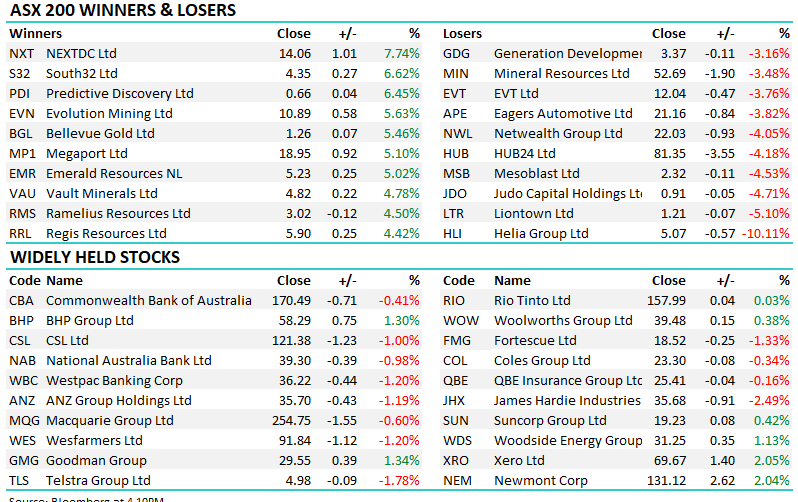

S32 -12.57%: A tough day for the diversified miner, flagging major impairments across two assets, calling out slightly soft 4Q24 production and downgrading FY25 production guidance – no good news there and the stock was rightly sold off. They said Aluminium was largely in line, though FY25 guidance was downgraded, Alumina missed and guidance was lowered for FY25, while they impaired Worsley Alumina (~US$554M pre-tax) and Cerro Matoso (~US$264M pre-tax) which will be recognised in FY24 results, the former being the main issue given its one of their flagship assets. Copper was a miss, but not a big surprise while Met Coal was inline with expectations, plus a few hits and misses elsewhere.

RE the Worsley issue, they noted that the WA Governments imposed environmental conditions create “significant operating challenges… and impact its LT viability”, clearly a concern. They will appeal, so more to play out here, however, it’s a large hit. On the more positive side, they expect completion of their Coal sale in 1QFY25 while they also talked about meeting cost guidance, and benefitting from some working capital unwind in 2H24.

- Weak update, big share price reaction, our feeling is that it’s overdone, however, we’ll let the dust settle before taking any action on our position.

MM remains long S32 in the Active Growth Portfolio

Add To Hit List