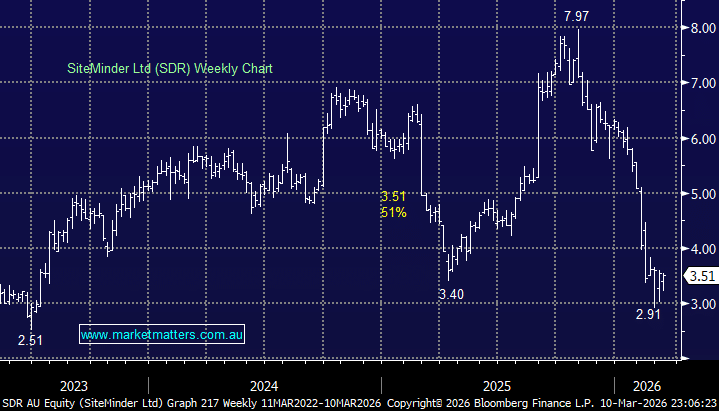

SiteMinder tells a similar story – quality business, punished share price – though the cause is different. Where Life360 was hit on a specific result, SiteMinder has been caught in the broader de-rating of smaller-cap SaaS names. The stock is now trading around $3.51, well below our entry point of $5.80 – a meaningful drawdown.

- We’ve tested our investment thesis on SDR half a dozen times, and we still strongly believe that it remains intact, and the selloff looks more like sentiment than fundamentals.

As a refresher, SiteMinder is cloud-based software for hotels i.e. the digital infrastructure that connects accommodation providers to the global booking ecosystem across Booking.com, Expedia, Airbnb and hundreds of other channels. Hotels use it to manage inventory, optimise pricing and maximise occupancy from a single platform. It’s sticky, it’s mission-critical, and it operates in a market that is still in the early stages of digitisation. Millions of properties globally are still running on legacy or manual systems, and we think the growth for SDR is obvious.

SiteMinder is still investing heavily in term of product, international expansion and building the platform out, and this has meant that near-term margin expansion has been slower than hoped, and the market has voted with its feet. But what hasn’t changed is SiteMinder’s scale and global reach, which are genuine competitive advantages. The platform connects nearly 50k properties across Europe, Asia-Pacific and the Americas to hundreds of booking channels. That creates real network effects. More hotels make the platform more valuable to distribution partners, which makes it more valuable to hotels. It’s a flywheel that gets harder to disrupt the larger it grows – a property cannot simply recreate that scale using cheap AI code!

More broadly, travel demand has remained resilient globally, and hotel operators continue investing in technology to improve yield and efficiency. SiteMinder sits directly in the path of that spending. The SaaS operating leverage story is still ahead of them. As the platform scales, incremental revenue should flow increasingly to the bottom line. The market is currently pricing SiteMinder as though the investment phase never ends. We don’t think that’s right.

- At current levels, the stock is pricing in a lot of pessimism for a business that continues to execute, operates in a structurally growing global market, and carries a genuine competitive moat. We remain comfortable holders and, like 360, are looking to add to our position.

MM is looking to add to SDR ~$3.50

Add To Hit List

Both stocks have been de-rated for reasons that feel more cyclical and sentiment-driven than structural. Both are growing revenues strongly, investing sensibly for the long term, and operating in markets with significant runway ahead. Neither is cheap on near-term earnings multiples, but that’s not the right lens for businesses at this stage of their growth curve.

For patient investors with a medium-term horizon like MM, the current weakness in both names looks like an opportunity to us. We’re looking to add to both positions, along with other portfolio holdings given current cash levels are sitting ~20%, with specific focus on Catapult (CAT), having trimmed above $7, Nick Scali (NCK) & ARB Corp (ARB).