SGH Ltd (formerly Seven Group Holdings) is a diversified industrial investment company with major interests in mining services, construction equipment, energy and media assets. In FY25, the company’s revenue came from four areas:

- WesTrac: the authorised Caterpillar equipment dealer for Western Australia, New South Wales, and the ACT ~54%.

- Boral: Australia’s largest construction materials company, supplying cement, concrete, asphalt and quarry products ~31%.

- Coates: Australia’s largest equipment hire company, supplying machinery, tools and specialist solutions ~9%.

- Energy: through its 30% stake in Beach Energy (BPT), and subsequent dividends ~6%.

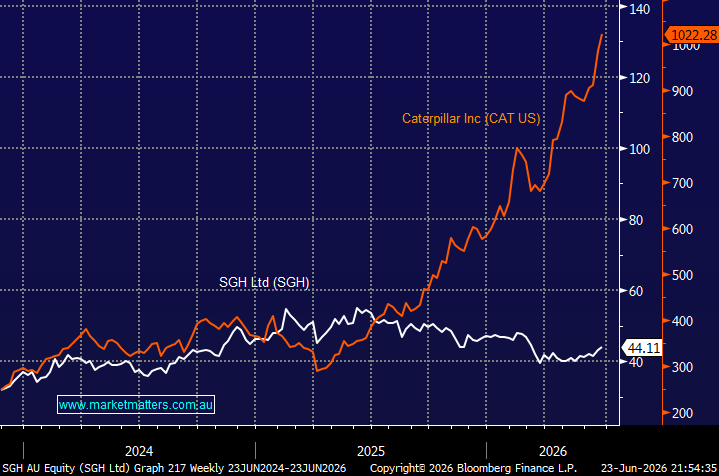

On Monday, SGH announced a $500 million on-market buyback, with the stock jumping 3% on the news. The program will commence around mid-August, coinciding with the FY26 full-year results and the end of the current trading blackout period. As the chart below shows, investors in SGH, with its significant exposure to Caterpillar, haven’t reaped the same rewards as those that simply bought the US name; unfortunately, the story of too many pockets of the ASX over the last 12-months.

The buyback is significant for two reasons: its sheer size and the likelihood that the Stokes family, which controls around ~51% of SGH, will not sell into the program. If they sit on the sidelines, the effective benefit to minority shareholders is magnified considerably.

- We feel that the buyback could be the perfect catalyst to trigger some performance catch-up by SGH (SGH) v Caterpillar (US CAT).

chart

SGH Ltd (ASX: SGH) v Caterpillar (NYSE: CAT)

chart

SGH Ltd (ASX: SGH) v Caterpillar (NYSE: CAT)

SGH used last month’s investor day to almost pat itself on the back, as it reinforced why the company has been such a strong long-term performer, highlighting a decade of disciplined execution that has delivered compound earnings (EBIT) growth of 18% per annum. Management was keen to emphasise its portfolio of quality assets, which are hard to replicate, protected by barriers to entry, and benefit from through-cycle resilience. Looking ahead, management is targeting 10% annual growth in both earnings and EPS over rolling three-year periods, a goal that sits well above current market expectations.

The outlook remains supported by resilient mining activity, ongoing infrastructure spending and growing energy demand, while management continues to see opportunities to improve profitability across WesTrac, Boral and Coates. SGH also expects AI initiatives and first gas from the Crux project in 2027 to provide additional growth avenues over the medium term.

However, we believe the key for SGH moving forward what they buy, given the company’s strong balance sheet, which could provide the business with another growth pillar – management has been explicit that the $500 million buyback will not constrain its ability to pursue inorganic growth opportunities at scale. Earlier in the year, they bid for BlueScope Steel (BSL), which was rejected, but it demonstrated both their intent and unwillingness to chase opportunities. We are fans of Ryan Stokes & Co, believing if and when they do press the M&A button, they’ll do it in a way that will be beneficial to shareholders.

- We can see SGH retesting its ~$56 high in 2026, especially if it makes a successful value accretive acquisition – we have added SGH to our Hitlist.

MM is bullish towards SGH around $44

Add To Hit List