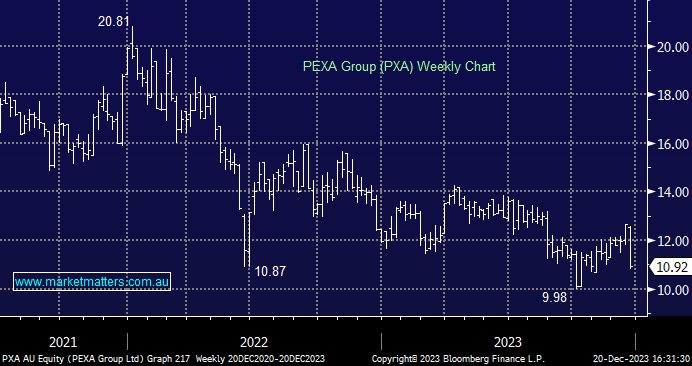

PXA -11.79%: provided updated guidance ahead of their acquisition of Smoove acquisition in the UK which will complete tonight. Cost control has been solid, helping the company stick to EBITDA margin guidance of 35%, however, revenues have lagged expectations across the three business streams. Refinance activity dropped from 28% in Q1 to 22% in the first 2 months of Q2, overall transaction growth has been modest and market share lost in international has not been recovered which is expected to cause a 10-14% drop in revenue in the first half vs 2H23. Overall, the company expects Group EBITDA to be $54-58m in the first half, and $109-115m in the FY before taking into account the expected $4-6m drag from the acquisition.

MM remains long and bullish PXA

Add To Hit List