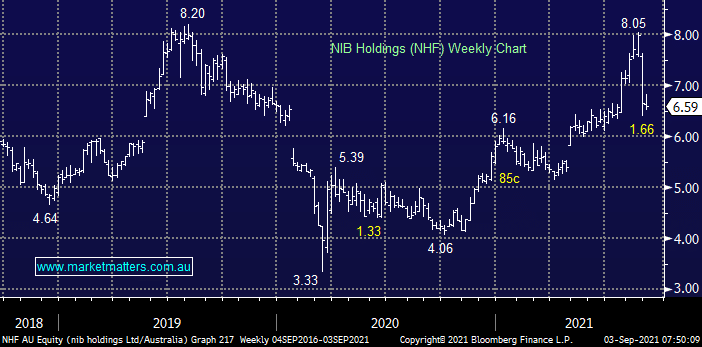

NHF disappointed investors last month after missing profit expectations by ~5% although the downside 20% rerating of the stock was largely because of the very conservative rhetoric towards next year citing last year as abnormally good given the pandemic tailwinds – interestingly if this is to be believed then MPL is trading too rich, or perhaps NHF is now cheap – we will consider this next.

We like the risk / reward towards NHF around the $6.50 area with its estimated more than 6% fully franked yield clearly appearing.

MM is neutral / bullish NHF

Add To Hit List