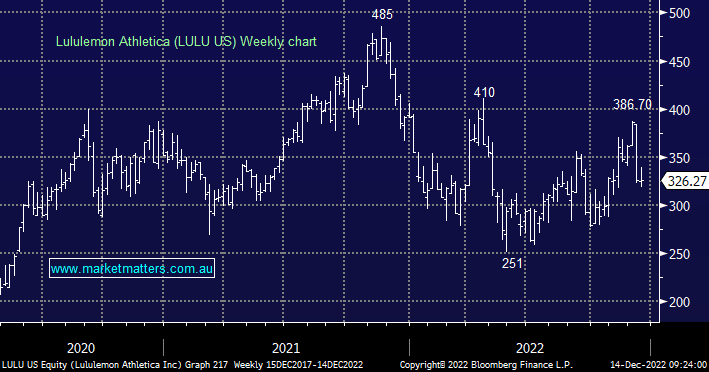

The designer and retailer of activewear has been on the MM Hitlist for a few months with the risk/reward unappealing as it traded near 12-month highs, defying the negative sentiment more broadly in retail. Last week, the stock dropped more than ~12% following their quarterly update that showed strong revenue and sales in Q3, but their guidance was softer-than-expected for the rest of the year. They simply think consumers will be hurt by higher interest rates driven by inflation – arguably a call anchored in the rear-view mirror!

In terms of guidance, they expect the next quarter’s net revenue to be in the range of $2.605bn to $2.655bn, as opposed to the previously projected $2.649 billion – a slight dip. That translates to earnings share (EPS) expected to be between $4.20 to $4.30 for the fourth quarter, compared to estimates of $4.30, a small decline and one that is worth looking through in MM’s view. While the short-term momentum is down for Lulu, we see good risk/reward ~US$320 leaving room to average on any move below $US300. This is a high-quality global retailer that is growing strongly.