LNW posted a solid set of numbers last week that reinforced our positive view on the stock. Group revenue dipped slightly (-1% YoY to $809m), but the underlying story was all about margins and earnings. For the half (They are December year-end), LNW reported:

- Adjusted earnings (Ebitda) up 7% to $352m

- Net profit jumped 16% to $135m

- Earnings per share (EPS) of $1.58 comfortably beat expectations.

Gaming remains the engine room with over 9,000 units sold globally, while SciPlay continues to outperform peers and iGaming delivered record quarterly revenue. The Grover Gaming acquisition is already paying its way, adding $21m revenue and broadening the platform.

Capital management was another highlight – $266m returned in 1H25 with the buyback program lifted to $1.5b. Management reaffirmed FY25 underlying Ebitda guidance of around $1.4b (inline with consensus) and reiterated longer-term targets of $2b Ebitda by 2028 (market is at $1.8bn), alongside a doubling of underlying net profit per share. The planned shift to a sole ASX listing by year-end should boost local investor engagement and liquidity.

- Overall, margins are moving in the right direction, cash returns are flowing, and omni-channel growth (Gaming, iGaming, SciPlay) remains strong. We remain positive on LNW, with the stock offering a clear runway to earnings growth and capital returns over the next few years.

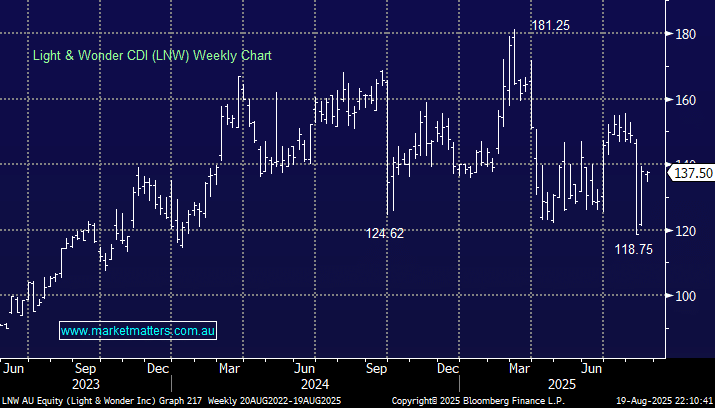

MM is bullish LNW, keeping it on the Hitlist

Add To Hit List