JBH and a number of other discretionary retail stocks were under pressure yesterday following the Fair Work Commission’s decision to lift minimum and award wages by 4.75% from 1 July. The move impacts around 2.8 million workers and has clear implications for labour-intensive sectors such as retail, hospitality and services.

The immediate market reaction was understandable. Higher wages mean higher operating costs, particularly for retailers with large store networks, weekend trading, casual labour and already tight margins. For companies like JB Hi-Fi, Harvey Norman, Super Retail, Premier Investments, Myer and Nick Scali, the concern is that wage inflation adds another layer of pressure at a time when consumers are already cautious, competition is intense and cost-of-doing-business pressures remain elevated.

The bigger macro concern is that stronger wages could also make the RBA’s job harder. Higher labour costs can flow through to prices, particularly in services and labour-heavy industries, while stronger wage growth risks keeping inflation above the RBA’s 2–3% target band for longer. This is particularly important for retailers because the last thing the sector needs is another leg higher in interest-rate expectations, given household budgets are already stretched by mortgage costs, rents, insurance and utilities.

However, there are some offsets that should not be ignored. Higher minimum and award wages also put more money into the pockets of lower-income workers, who generally have a higher propensity to spend. That can support demand across everyday discretionary categories, including electronics, appliances, mobile phones, gaming, computers and other household items – areas where JB Hi-Fi and The Good Guys are particularly well positioned.

In other words, the wage increase is not purely negative for JBH. It lifts costs, but it can also support revenue if the extra income flows back into consumption. JB Hi-Fi also has several advantages relative to many retailers: strong brand recognition, scale, efficient store economics, a value-based customer proposition and exposure to product categories that are increasingly viewed as essential rather than purely discretionary. Phones, laptops, appliances and connected devices are no longer luxury purchases for many households.

The key issue is whether JBH can absorb higher labour costs through sales growth, supplier support, productivity gains and operating leverage. Historically, JB Hi-Fi has been one of the best operators in Australian retail, with a strong track record of managing margins through changing cycles. That does not make it immune to wage inflation or a weaker consumer, but it does mean the market should be careful not to treat all retailers the same.

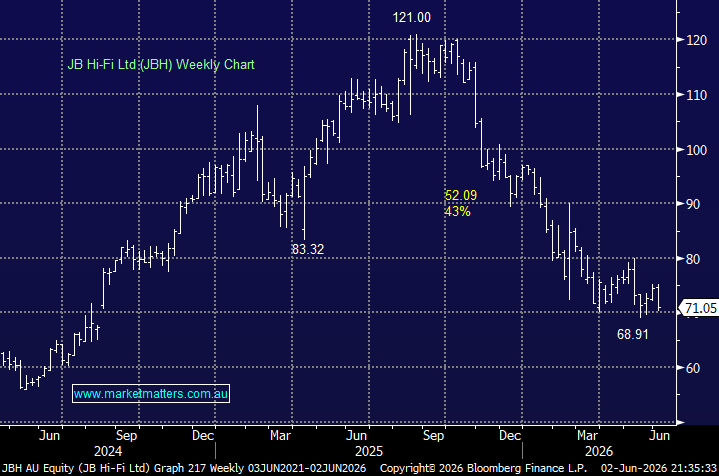

We understand yesterday’s weakness. Higher wages add to margin pressure and increase the risk that inflation remains sticky, keeping the RBA in a hawkish frame of mind. However, for a high-quality retailer like JB Hi-Fi, there is also a demand offset from stronger household incomes, particularly in its key categories. The near-term macro backdrop remains challenging, but we would not be surprised to see JBH outperform weaker retail peers as investors become more selective.

- We believe the recent aggressive sell-off in discretionary retail stocks, exacerbated by yesterday’s move on wages, is still presenting a solid opportunity in some of the higher-quality names in the sector – such as JB Hi-Fi.

MM remains long & bullish JBH ~$71

Add To Hit List