JHX -0.86%: Posted a solid fourth quarter update however FY27 guidance came in slightly below expectations, with softer assumptions around US housing activity and weather disruptions weighing on sentiment despite a resilient underlying result.

4Q Highlights:

- Net sales: $4.84bn vs $4.84bn estimate

- Adjusted net income: $595.7m, -7.5% y/y vs estimate $595.9m

- FY27 EBITDA guidance: $1.45–1.50bn

- FY27 free cash flow guidance: >$500m

The key disappointment was FY27 guidance, with the midpoint of EBITDA expectations landing modestly below consensus as management assumed the US repair and remodel market declines ~2% through the year.

That said, operationally the result was still solid. Management highlighted strong execution in a difficult environment, noting underlying performance exceeded expectations despite construction disruption and softer housing conditions.

While the AZEK decking business numbers were softer than expected due to weather conditions, integration and cost synergies from the acquisition are still tracking ahead of schedule.

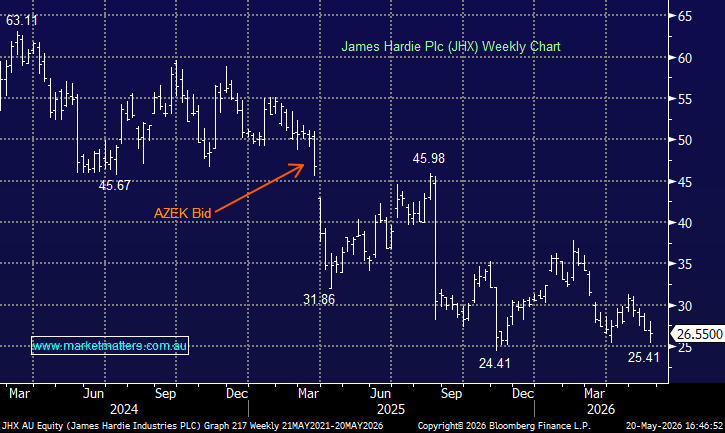

MM remains long and bullish JHX

Add To Hit List