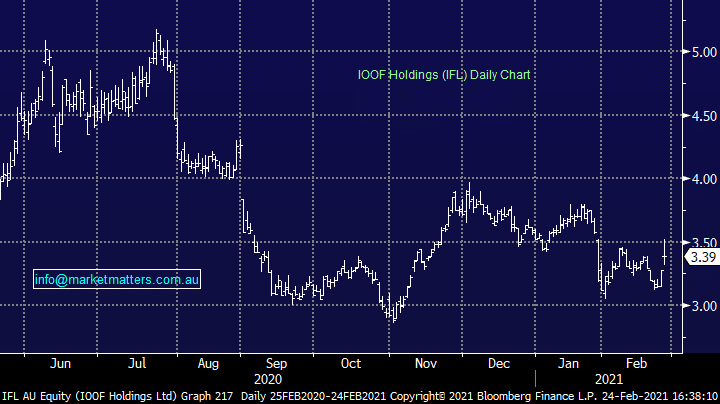

The beaten up wealth manager reported 1H21 results this morning that were okay, and an okay result was all they needed to deliver to see the stock higher. Underlying profit was $65.9 million, up +7.4% yoy and they reported an interim dividend of 8c plus a special dividend of 3.5c. That’s 11.5c for the half or nearly 7% annualised, which is strong. The be optimistic on IFL we need to believe in their strategy of using technology to scale financial planning, reducing its cost and complexity and improving it’s accessibility, of course while still making money. For MM, the jury is still out on their strategy hwoever the stocks cheap enough around current levels to give them the benefit of the doubt.

We view IFL as a cheap turnaround play, offering a solid yield while we wait.

Add To Hit List