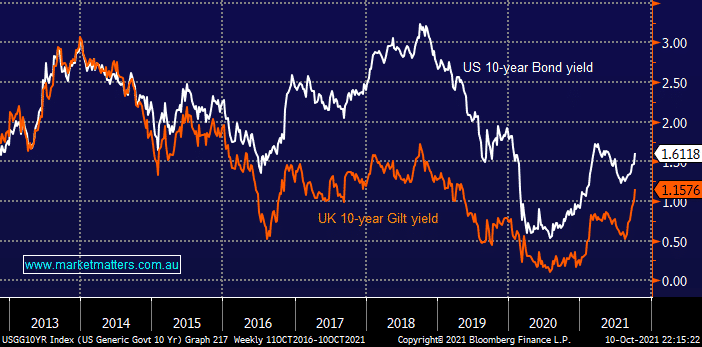

No change, local bond yields have continued to rise from their late August low, the RBA may be sticking to its guns to hold the cash rate at 0.1% through until 2024 but markets are voting on rate hikes moving forward with the only point of debate being when, not if. Whether we look to Europe, the US or across the Tasman the picture is the same with yields rising:

- UK yields are already trading on 2-year highs with our own and US not far behind.

- Inflation expectations across much of Europe are now at the highest levels since the GFC, more than a decade ago.

At this stage the economic picture is not as robust with yields being driven by the likes of rising oil prices but if / when we see activity lift, rates could accelerate higher which is what we feel the RBA is nervous around with regard to the Australian housing market. However for now the scribes looking for a negative shock story have started discussing stagflation but a few bad employment prints such as the one we saw in the US on Friday doesn’t herald the start of a slowdown, hopefully more like a bump in the road – this is definitely not a scenario to be dismissed but it’s not our preferred path.

NB Stagflation is when inflation rises as the economy contracts, a very bad backdrop for equities with the last major example being in the 1970’s.

MM remains bullish bond yields from current levels into 2022

Add To Hit List