HCA Healthcare (HCA US) fell -6.95% overnight after the hospital operator released preliminary second-quarter results early and lowered its FY26 earnings guidance, with a sharp deterioration in payer mix and softer surgical volumes weighing on the outlook.

Preliminary 2Q26 results:

- Revenue of US$20.23bn, ahead of Bloomberg consensus at US$19.42bn

- Adjusted EBITDA of US$4.03bn, broadly in line with the US$4.0bn expected

Revised FY26 guidance:

- EPS of US$28.70–30.50, down from US$29.10–31.50

- Adjusted EBITDA of US$15.4–16.1bn, down from US$15.55–16.45bn

- Revenue of US$77–79.5bn, compared with prior guidance of US$76.5–80bn

- Capital expenditure maintained at US$5–5.5bn

The key issue was an adverse payer mix shift, driven by a larger-than-expected increase in uninsured patients after people lost coverage through the US health insurance exchanges. HCA estimates the deterioration will negatively affect FY26 pre-tax income by around US$400m, materially more than initially anticipated.

Operating trends were also softer than expected, with same-store inpatient surgical volumes falling 2.3% and outpatient surgeries declining 3.4%. This compounded the reimbursement pressure, given surgical procedures are generally among the more profitable services provided by hospital operators.

The weakness spread across the broader healthcare sector in the US, with Tenet Healthcare, Universal Health Services and Community Health Systems all declining, while medical-device manufacturer Smith & Nephew also traded lower on concerns around softer surgical volumes.

This was clearly a disappointing update, particularly because the guidance reduction was driven by both reimbursement pressure and weaker underlying procedure volumes. The adverse payer mix is meaningful and may remain difficult to forecast while health insurance coverage remains under pressure.

However, the result was not weak across the board. Revenue remained strong, EBITDA was broadly in line with expectations, and HCA continues to generate substantial cash flow while investing US$5–5.5bn annually across its hospital network. The structural appeal of the business also remains intact, underpinned by strong regional market positions, scale advantages and long-term demand for healthcare services.

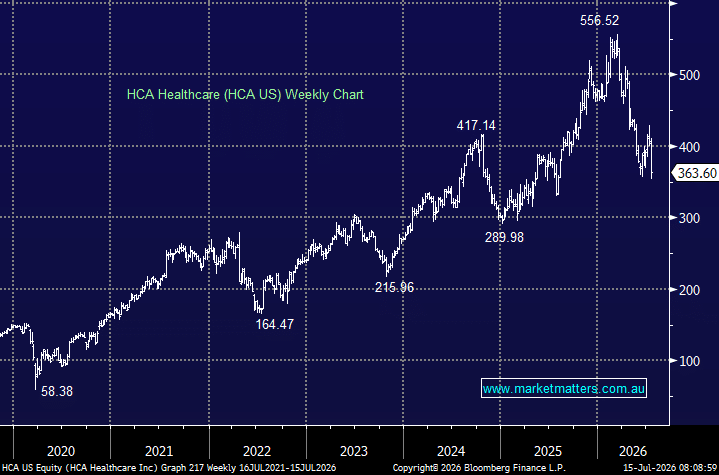

We recently added HCA to the International Equities Portfolio at ~$392 following a ~30% pullback in the shares, and despite today’s update, we do not believe the long-term investment case has been broken. The key question is whether the payer-mix deterioration is a temporary reset or the beginning of a more persistent earnings headwind, and we’ll need time to assess that.

MM remains positive on HCA ~$363

Add To Hit List