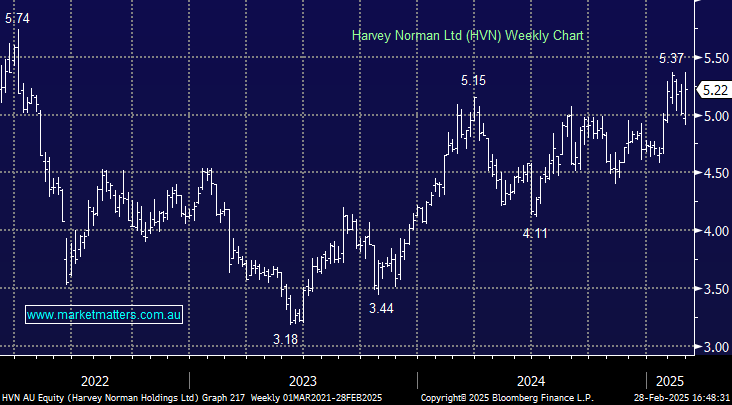

HVN +2.55%: Was a top performer on the ASX today (slim pickings) as 1H25 results impressed, the stock going against the grain and moving higher on stronger than expected franchise (store) earnings and solid sales momentum into 2H.

- 1H25 $2.29bn consolidated revenue

- 1H25 profit before tax (PBT) $312 million, 1% above consensus

- 1H25 Franchise PBT $180.2m, 5% above consensus

The solid earnings in 1H look to have continued into the second half. Same-store-sales growth sat at 2.1% in January which compared poorly to Good Guys at 5.9% for the same period. However, HVN looks to have kicked it up a notch with 7% growth for the 21 days of February.

Management did announce the rollout of 80 stores in Malaysia will be pushed back from 2028 to 2030 which casts doubt around their international growth strategy. For now, the market is more focused on near-term earnings, which are proving resilient.

MM is bullish HVN

Add To Hit List