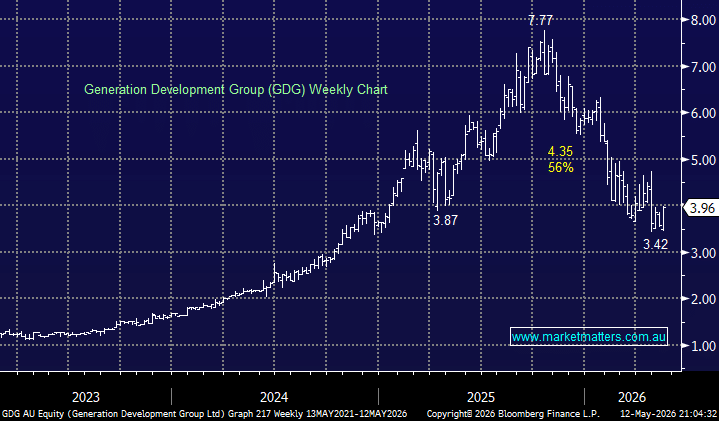

GDG has moved dramatically from a small cap hero to one plumbing level’s last seen in 2024 as their rate of growth in managed accounts trailed bullish market expectations while costs have also been elevated. Shares have more than halved from a ~$7.70 high this year to close yesterday below $4.

As a refresher, GDG is a wealth management and investment solutions business focused on tax-effective long-term savings products and adviser-led portfolio solutions. Its core business, Generation Life, provides investment bonds, lifetime annuities and other tax-aware structures used for wealth accumulation, estate planning and retirement income, while Evidentia / Lonsec Investment Solutions provides managed account and implemented portfolio solutions to financial advisers. In simple terms, GDG helps advisers and investors access professionally managed, tax-effective investment structures, with earnings driven by funds under management, inflows and platform/adviser adoption.

- While we don’t own GDG, changes to the tax treatment of capital gains released in the budget overnight should be a net positive for the business.

The announced removal of the 50% Capital Gains Tax discount, replaced by an inflation-indexing model reduces the relative attractiveness of assets where investors have historically relied on discounted capital gains. GDG’s investment bond offering is a likely beneficiary because investment bonds are taxed internally at up to 30%, with no distinction between income and capital gains.

In simple terms, as the tax benefit of holding assets personally or through other structures is reduced, tax-paid structures like investment bonds look more appealing for long-term investors, estate planning and intergenerational wealth transfer. That does not mean demand turns on overnight, but it does improve the structural tailwind behind the business.

The investment bond market is still relatively underpenetrated in Australia, and Budget-driven tax changes we think will become a useful education and distribution catalyst for advisers. GDG is also becoming more than just an investment bond business. The recent migration of $1.8bn in Xplore Wealth MDA portfolios to Evidentia Group’s Implemented Portfolios on the HUB24 platform lifted Implemented Portfolios’ total FUM to more than $4bn.

- Implemented portfolios and managed account solutions remain a clear growth area across the advice market, as advisers look for more scalable and compliant ways to manage client portfolios. GDG’s exposure here gives it another growth lever beyond investment bonds.

The market remains bullish on the stock – and has done during its 50% re-rate lower. Consensus shows all buy ratings (8), and an average 12-month target price of around $6.24, implying upside of roughly 58% from the current price. Forecasts also imply continued earnings growth, with adjusted EPS expected to rise from around 10.4c in FY26 to 13.3c in FY27 and 17.0c in FY28, while revenue is forecast to grow from about $170m in FY26 to $245m in FY28. That growth profile is attractive, though the stock is not cheap, trading on roughly 38x FY26 earnings, falling to around 30x FY27 and 23x FY28.

The valuation is the main sticking point. GDG has a good thematic tailwind, a strong market position, and is a clear potential budget beneficiary, but a lot of growth is already being assumed. It is a high-quality thematic exposure to the evolution of wealth management in Australia, but at this stage we would prefer to see either a better entry point or more evidence that the Budget tailwind is translating into stronger flows. We are adding GDG to the Hitlist.