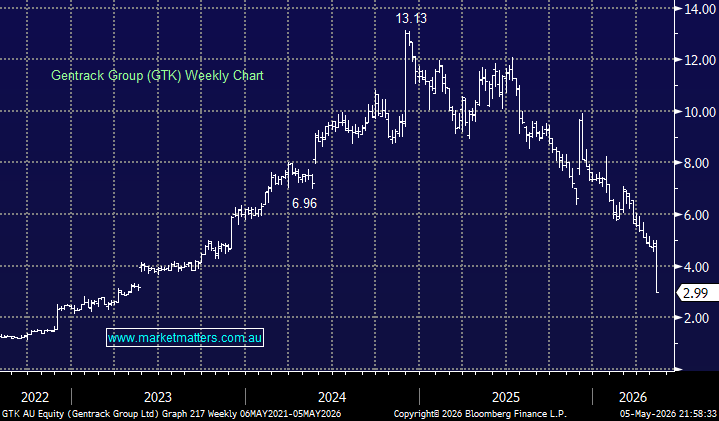

Gentrack (GTK) was smashed yesterday, down 38% after downgrading FY26 guidance. We have looked at GTK in the past – and we even called it “one that got away”, however yesterday’s update was weak, and the reaction was brutal.

Looking at GTK from a wider lens, we like the broad thematic exposure – software for utilities and airports, sticky customers, rising recurring revenue and a global growth runway, but yesterday’s update was a clear reminder that valuation matters, particularly when a high-multiple growth stock starts missing numbers.

The headline disappointment was guidance. GTK now expects FY26 revenue of $229–238m, around 9% below consensus, with FY26 EBITDA now expected to be just $13.5–20m (excluding acquisition costs), which is a far cry from the $33.5m expected (~50% lower). 1H revenue is expected to be around $110m, with 1H EBITDA of only $7.8m.

The company is blaming weaker non-recurring revenue, while also saying it is deliberately prioritising long-term growth, international expansion and product development over near-term profitability. There is a more positive read-through beneath the downgrade. Recurring revenue is expected to grow by more than 10% to around $174m, which is a better-quality revenue base than one-off implementation work. The move toward g2.0 should, in theory, reduce customer onboarding costs, increase recurring revenue and improve scalability over time. Management also reiterated its medium-term target of more than 15% revenue CAGR, which implies the longer-term ambition has not changed.

The problem is trust. When a growth company asks the market to look through a sharp earnings reset and focus on medium-term targets, investors need confidence that today’s weakness is a transition issue, not a demand issue. GTK is saying the shift is strategic, lower non-recurring revenue today in exchange for higher-quality recurring revenue tomorrow, but we’ve heard that before from other companies in a similar position. The 1H result on 18 May 2026 is important, particularly around customer wins, pipeline conversion, churn, cash flow and whether the lower margin profile is temporary.

They have proposed a $20m on-market buyback, which is a useful signal from the board, particularly given management says it is supported by a strong balance sheet and will not compromise growth investment. However, buybacks do not fix earnings downgrades. They can help support the share price, but they are not a substitute for rebuilding confidence in forecasts and execution.

Overall, GTK is now more interesting after today’s sell-off, but we would not be rushing in purely because the stock is down ~40%. The business still has appealing long-term attributes, sticky customers, growing recurring revenue, global expansion potential and exposure to utilities and airport software, but today’s downgrade makes it a risky proposition.

The market will now value GTK less on the dream and more on delivery. We are adding it back on the Hitlist for the Emerging Companies Portfolio, but will await the 18 May result, and look for evidence that recurring revenue growth is ticking up, margins can be rebuilt, and the g2.0 transition is genuinely creating a better business rather than masking a softer demand environment.

- For now, it is one to watch, but we don’t have any plans to catch this falling knife.

MM is adding GTK to the Emerging Companies Hitlist

Add To Hit List