GTK has now reported its 1H26 result, following the sharp guidance downgrade that saw the stock fall heavily early last month. At the time, we said GTK was more interesting after the sell-off, but we were not inclined to catch a falling knife until the result provided more evidence around recurring revenue, customer wins, cash flow and margins.

The result was largely in line with the pre-announced numbers, which is important. There was no further downgrade, and while the earnings reset remains significant, the stock has moved from being priced for perfection to pricing in a lot more bad news.

GTK reported 1H26 revenue of ~$110m, down 2%, and EBITDA of ~$8m, in line with the earlier update. Weakness was concentrated in Utilities non-recurring revenue, which fell 33% as project work was deferred and the business shifts towards lower upfront implementation revenue and a greater recurring revenue mix. Utilities recurring revenue still grew 9%, while Airport recurring revenue grew 33%, with Veovo margins remaining strong.

UBS has upgraded GTK to Buy, albeit with a much lower NZ$4.70 price target, down from NZ$9.65. Its view is that the current share price is now taking an overly pessimistic view of the Utilities business, while 2–3 new customer wins over the next nine months could help shift the narrative from an earnings reset to a rebuilding growth story. UBS has still cut forecasts materially, lowering FY26, FY27 and FY28 EBITDA estimates by 48%, 39% and 42%, reflecting slower international expansion, lower project revenue and higher investment in sales, R&D and AI.

The bull case is that GTK is deliberately sacrificing lower-quality, lumpy implementation revenue today in exchange for a higher-quality recurring revenue base tomorrow. The bear case is that this is not just a transition issue, but evidence of slower demand, tougher competition and a more expensive global expansion path.

Competition remains a key risk, particularly from Kraken, which appears strong in B2C utility billing. GTK’s relative strength is more in B2B and complex utility environments, and the acquisition of Factor for ~$24m makes strategic sense in that context, adding commercial energy pricing and contract management capability into G2.

We are less concerned about AI as an immediate existential threat. Utility billing systems are complex, regulated and deeply embedded, making them difficult to replace quickly- this is the type of software business we are drawn to. AI is more likely to become a feature that improves workflow, pricing and customer service than a near-term replacement for the core system. However, GTK must keep investing here, otherwise AI could become a pricing or retention risk over time.

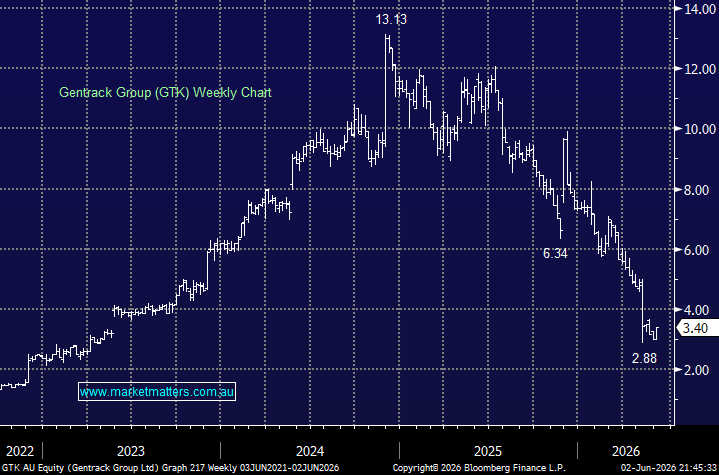

Overall, GTK has moved from “too expensive and too risky” to “speculative but interesting.” The 1H result did not fix the downgrade, but it did confirm that the worst of the reset was already known. The valuation is a lot more palatable, the recurring revenue mix is improving, and the buyback provides some support.

- We are now becoming more interested in GTK and see current market pricing as being too bearish for the quality of the business.

The stock has been crucified on the above-mentioned risks, and with some improving sentiment towards the software complex, we believe the risk/reward now looks attractive.

MM has turned bullish on GTK ~$3.50

Add To Hit List