What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

Firstly, for the absent-minded subscriber, remember it’s Valentine’s Day!

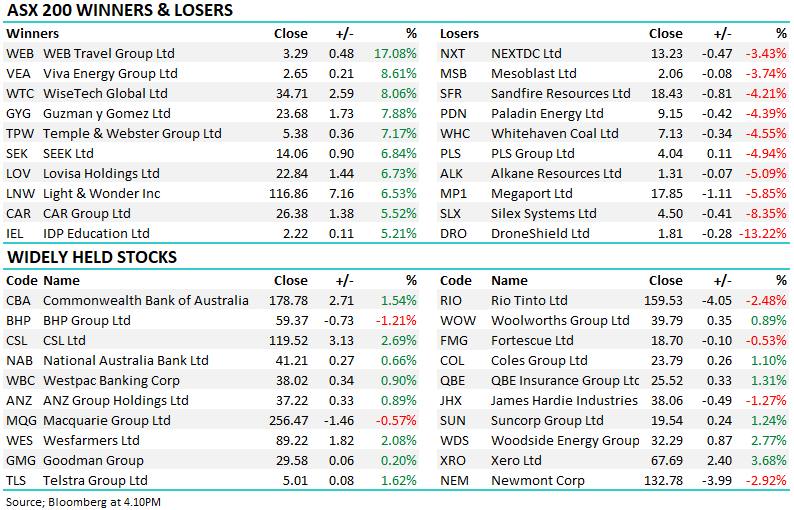

Yesterday’s earnings numbers largely disappointed the market, with moves likely amplified by “crowded positions” after more than a year where the trend has been the investor’s friend. On Tuesday, we wrote, “We are constantly questioning and re-evaluating our views, and at this stage, MM is still working off the opinion that 2024 will be a year of reversion” – one day doesn’t make a summer, but it caught our attention how many outperformers found themselves in the “naughty corner” on Tuesday and vice versa:

Winners: Challenger Ltd (CGF) +8.4%, West African Resources (WAF) +4.2%, Credit Corp (CCP) +3.2%, Healius (HLS) +3.2%, and IDP Education (IEL) +3.1%.

Losers: James Hardie (JHX) -8.5%, Megaport (MP1) -2.8%, CSL Ltd (CSL) -2.8%, CAR Group (CAR) -2%, REA Group (REA) -1.7%, and Altium (ALU) -1.4%.

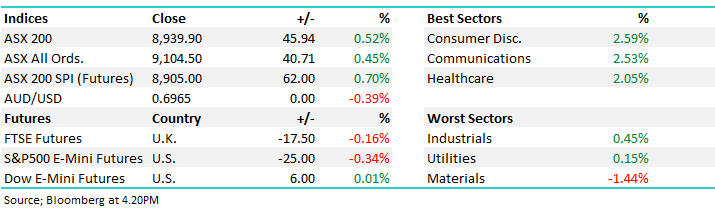

Overnight US markets sold off aggressively after a hotter-than-expected CPI inflation read left the optimistic Doves near-term rate cut hopes in tatters. Bonds and stocks both slid following the release, which climbed the most in eight months just when investors were expecting confirmation that inflation is under control; the US 2s climbed back to levels not seen since the December central bank “pivot” – another example of crowded positioning coming under pressure. The release added credibility to Jerome Powell’s “wait-and-see attitude”, with the futures now pricing in a Fed Funds rate of ~4.45% by Christmas, around four cuts.

- After such a strong advance by the “Magnificent Seven”, a 10% pullback would hardly register on the chart.

MM is looking for performance reversion through 2024

Add To Hit List

The ASX200 is experiencing plenty of volatility on the stock/sector level as earnings season keeps the market on its toes, but on the index level, things are pretty steady, with the last ten sessions spending most of their time rotating between 7600 and 7700. The influential banks have been firm in 2024, largely counter-balancing weakness in the miners while the rest of the market has danced to its own tune. Our preferred scenario is the index consolidates with a downward bias over the coming weeks, but as we’ve already witnessed beneath the hood, there’s likely to be plenty of winners & losers whatever path the index takes.

- MM is in “buy mode”, having moved to a defensive stance over recent weeks, but isn’t in a hurry to deploy cash just yet.

- This morning, the SPI Futures are pointing to a sharp drop by the ASX200 on the opening, down around -1.2%.

MM is now neutral toward the ASX200 short-term

Add To Hit List