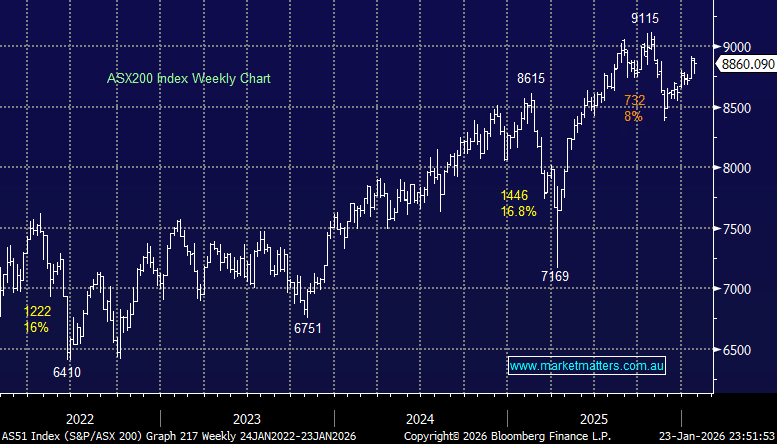

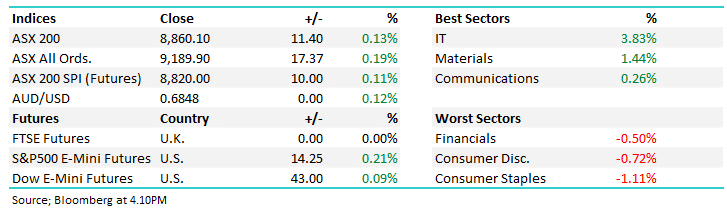

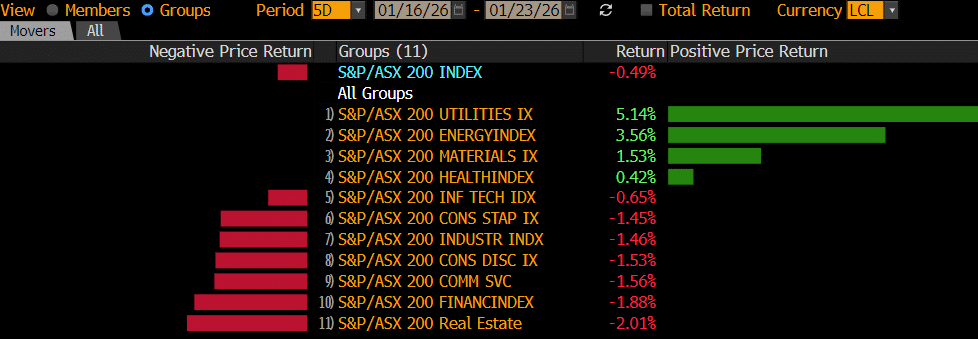

The ASX 200 finished a choppy week down just -0.5%, recovering from early weakness sparked by President Trump’s threats toward European allies tied to his ambitions around Greenland. While the rhetoric was quickly walked back at Davos, the episode was a reminder of how abruptly geopolitical risk can re-emerge. Yet markets largely shrugged it off, highlighting their resilience to headline-driven volatility. The “buy-the-dip” trade — closely tied to the so-called “TACO trade” (Trump Always Chickens Out) — continues to deliver, at least for now. The market may feel unsettled to many, but it’s still up +1.7% year-to-date, dragged higher by a robust materials sector, which has already surged +9.3% in 2026.

On the stock level, there was pronounced volatility over the 5-days with 12 stocks rallying/declining by over 10%. The winners’ enclosure was dominated by uranium, lithium and gold names, while it was a more eclectic bunch in the naughty corner:

Winners: Paladin Energy (PDN) +19.8%, IperionX (IPX) +16.7%, Life360 Inc (360) +15.6%, Westgold WGX) +15.3%, Evolution Mining Ltd (EVN) +13.3%, Silex Systems (SLX) +10%, Pilbara (PLS) +8.6%, and Origin Energy (ORG) +7.2%.

Losers: ARB Corp (ARB) -18.6%, a2 Milk (A2M) -13%, Austal (ASB) -12.2%, Pro Medicus (PME) -10.8%, Light & Wonder (LNW) -9.7%, Orora (ORA) -8.4%, WiseTech Global (WTC) -7.7%, JB Hi-Fi (JBH) -5.2%, and ANZ Group (ANZ) -3.5%.

The market-focused news was dominated by President Trump & Davos, plus a sprinkling of domestic economic news:

- On Monday, global equities fell sharply as renewed tariff threats tied to Trump’s Greenland rhetoric reignited trade and geopolitical risk, ahead of the Davos (World Economic Forum 2026).

- On Wednesday night, the TACO trade resurfaced after Trump’s speech from Davos, when he said the US would not invade Greenland nor impose tariffs on European countries who did not support his approach.

- The ASX underperformed its peers on Thursday following hot employment data, which increased the chances of an RBA rate hike in February; credit markets have it priced as a more than 50% chance.

- The Australian Dollar ($A) was a huge benefactor during the week, challenging 69c on Friday, its highest level since late 2024.

- Spot silver surged ~7% on Friday, above $US100/oz, lifting year-to-date gains above 40% after prices more than doubled in 2025. Gold also pushed to a fresh record, edging closer to $5,000/oz, as demand was fueled by uncertainty around trade, geopolitics and monetary policy.

Overseas markets were relatively quiet and mixed as we went into the local long weekend. In Europe, the EURO STOXX 50 slipped -0.1% while the German DAX advanced +0.2%. In the US, the Russell 2000 small-cap index fell -1.8% while the tech-based NASDAQ advanced +0.3% amid renewed enthusiasm around AI, but overall US stocks fell for the 2nd consecutive week.

- The SPI Futures are calling the ASX200 to open up +0.1% next week with BHP up 50c in US trade, although this will change due to the public holiday.