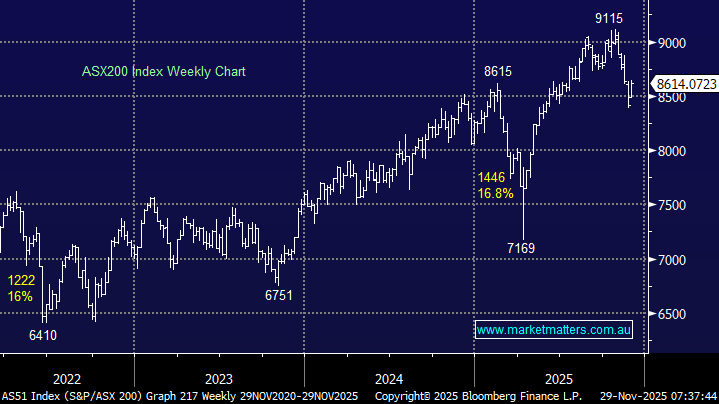

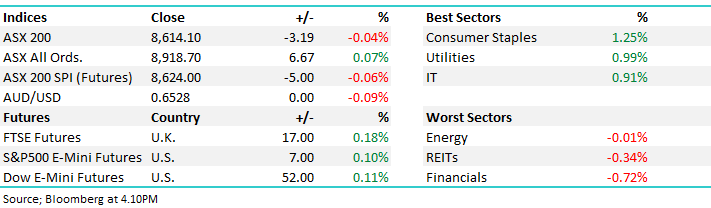

The ASX 200 bounced back +2.4% last week (though still ended November down 3%) following dovish comments from several Fed members. Gains were broad-based, with tech, materials, healthcare, and the industrial sectors all advancing by over 4%; only the Energy sector failed to advance. This week’s rise on the ASX came despite Wednesday’s higher-than-expected local inflation figures, which prompted speculation from some that the RBA may hike interest rates next year. Even so, the future path of Australian interest rates remains debated, and some market economists maintain the RBA could still cut rates from today’s level of 3.6% – MM believes there will be no change, just plenty of speculation until 2027.

By Friday’s close, the winners’ enclosure was dominated by takeover action and recovery action, whereas the losers’ names were mostly stocks that disappointed the market on the reporting front.

Winners: WEB Travel Group (WEB) +23.6%, National Storage (NSR) +20.4%, HMC Capital (HMC) +20.2%, QUB Holdings (QUB) +19.4%, Zip (ZIP) +19.3%, Catapult (CAT) +19.1%, Ramsay Healthcare (RHC) +17.7%, and Reece (REC) +15.8%.

Losers: Temple & Webster (TPW) -15.7%, Bendigo Bank (BEN) -6.1%, Suncorp (SUN) -6.1%, GrainCorp (GNC) -4.4%, Harvey Norman (HVN) -4.3%, (ELD) -2.9%, Liontown Resources (LTR) -2.4%, and Sigma Healthcare (SIG) -2.4%.

The global economic and geopolitical news was dominated by commentary from Fed members, increasing optimism that a rate cut is on the cards for December:

- At the end of last week, New York Fed President John Williams, often viewed as a bellwether for Powell’s thinking, signalled support for a rate cut, as did another Fed member Chris Waller.

- On Monday, BHP attempted for one last time to engage Anglo-American before quickly walking away.

- On Wednesday, Australia’s higher-than-expected inflation figures prompted analysts to start forecasting rate hikes in 2026 – we think unlikely.

- Throughout the week, we saw a plethora of M&A activity and company “misses” leading to some very polarised performance, illustrated above.

- US markets were closed on Thursday and had a shortened session on Friday, but it didn’t subdue the bulls, who are now looking for a rate cut in December.

- Futures markets are now pricing in a more than 80% chance the Fed cuts by 0.25% next month.

Overseas markets extended the strong week’s gains on Friday night in the shortened post-Thanksgiving Day session. The S&P 500 closed up +0.5% taking it back within striking distance of its all-time high. In Europe, the German DAX and UK FTSE both advanced +0.3%

- The SPI Futures are calling the ASX200 to open up +0.1% on Monday morning following strength on Wall Street into the weekend in the shortened session.