- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

*Apologies, no Afternoon Note was sent yesterday afternoon*

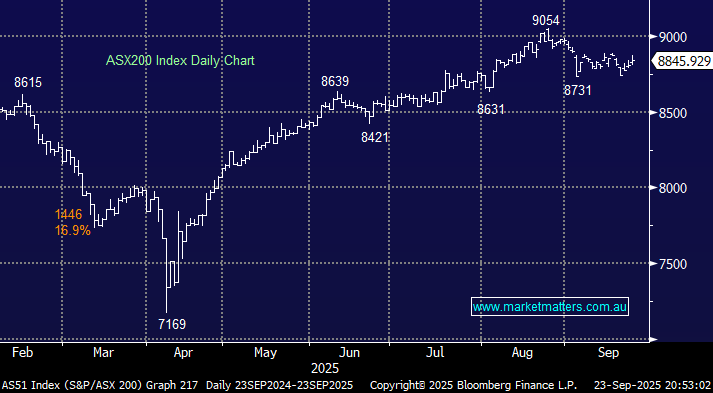

The ASX200 rose 0.4% on Tuesday, posting its 3rd consecutive gain, led by the financials and in particular the Big Four banks, which averaged a gain of ~0.8%. The materials sector was again strong, testing its 12-month high under the power of the large-cap iron ore miners and rampant gold market, which we will look at later, as China gave the precious metal another reason to charge higher. The local index has spent the last 3 weeks rotating in a tight ~1.8% trading range around the 8800 area, as gains by the influential miners offset losses in oil & gas, consumer staples and healthcare.

For the second month in a row, uranium stocks continued to show strength. On Tuesday, Paladin Energy (PDN) gained 2.4 % and enrichment technology company Silex Systems (SLX), which has soared more than 40% over the last week, edged higher to $6.03, and it still looks good – we own SLX in our Emerging Companies Portfolio. The sector has recently been boosted by news that global commodities trading giant Mercuria will expand into physical uranium, nuclear reactor restarts and supply cuts from the world’s largest uranium producer, Kazatomprom.

- September is, on average, the weakest month of the year, and it’s delivering again in 2025, the ASX200 has retreated 1.4% so far, despite the strong advance by the local miners and broad-based impressive gains on Wall Street.

- Looking ahead, October is, on average, the most volatile month of the year; over the last decade, the index has closed up or down over 3.75% once, 4% twice and 6% twice, with larger swings within these five volatile months.

If this year delivers another bout of volatility, which looks like a 50% chance going by the last decade, we plan to “buy the dip” if the moves on the downside, until further notice.

Overseas markets were mixed with a soft bias overnight after Fed Chair Jerome Powell suggested the market was overvalued, saying “ equity prices are fairly highly valued” while adding caution on the path for interest rates, signalling that the rate-cutting path wasn’t clear and that it was a “challenging situation”. In Europe, the EURO STOXX 50 gained +0.6% while the UK FTSE edged lower. In the US, the tech-based NASDAQ led the decline, falling 0.7% while the Dow finished down 0.2%.

- The ASX200 is set to open down 0.4% this morning, back around 8800 following weakness on overseas bourses.