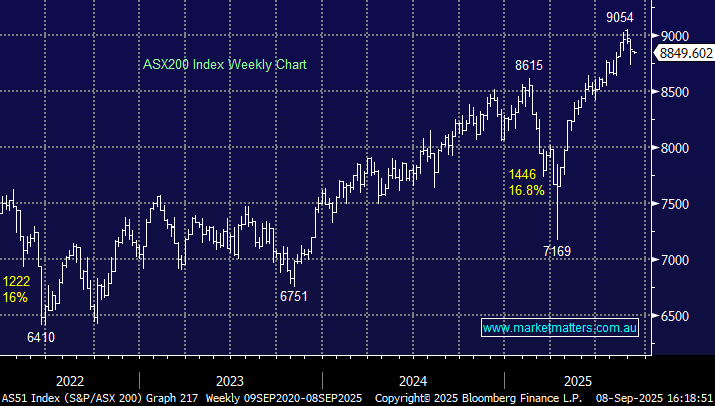

The ASX 200 slipped 0.2% on a muted Monday, with over half of the main board finishing lower. Financials and energy led losses, while tech and healthcare bucked the recent trend with a rare day of outperformance. September’s reputation as a seasonally weak month is holding true, with the index now down 1.4% month-to-date. Still, the wave of dividend payouts due in the coming weeks could provide investors with fresh capital to support the market.

- Losses were compounded on Monday by SmartGroup (SIQ), Super Retail (SUL), HUB24 (HUB), and AUB Group (AUB), all trading ex-dividend.

A couple of interesting moves on the stock/sector front, which might herald a change in short-term trends over the not-too-distant future:

- Woollies (WOW) bounced +0.5%, and Coles (COL) slipped -0.8% after a Fed court ruling, which implies the supermarket giants face a $1bn blowout to remedy staff underpayment for up to 28,000 managers going back to 2013.

- The gold price pushed new all-time highs, with the spot price breaching $US3600, yet most gold stocks actually drifted lower, including Ramelius (RMS) -1.5%, Evolution (EVN) -1.4%, and Newmont (NEM) -0.6%.

Overseas markets started the week in positive fashion as optimism around the looming Fed rate cut gathered momentum. In Europe, the EURO STOXX 50 and UK FTSE gained +0.8%. In the US, the S&P 500 added +0.2%, whilst the NASDAQ closed +0.5% higher as Nvidia (NVDA US) enjoyed a day back in the winners’ enclosure +0.8%.

- The SPI futures are calling the ASX200 to open down 0.3%, ignoring the strength on overseas bourses.