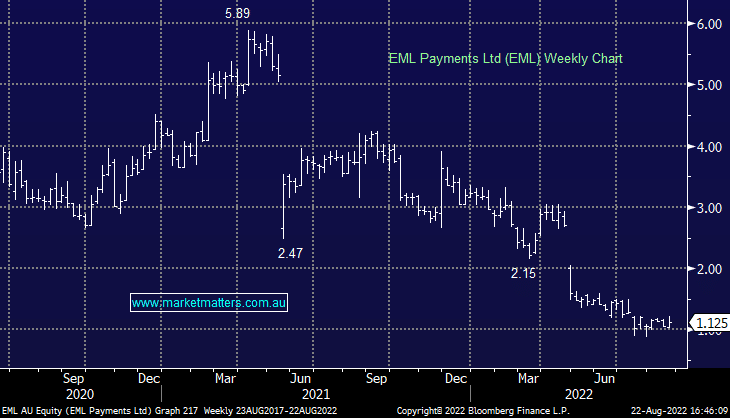

EML +6.13%: FY22 results today showed better than expected top-line growth but a challenging year from a remediation/cost perspective. This is not a bad result given ~60% of their business is in Europe, which is experiencing some big macro headwinds. Revenue from ordinary activities came in at $232.4m, a touch ahead of $230.5m expected while underlying EBITDA of $51.2m was a beat to $48m consensus. They launched a relatively small on-market share buy-back program of up to $20 million and said cash was sitting at $73.7m. The question being, has peak pessimism past for EML and is there more corporate interest out there – we suspect there is.

MM is looking for further corporate interest in EML

Add To Hit List