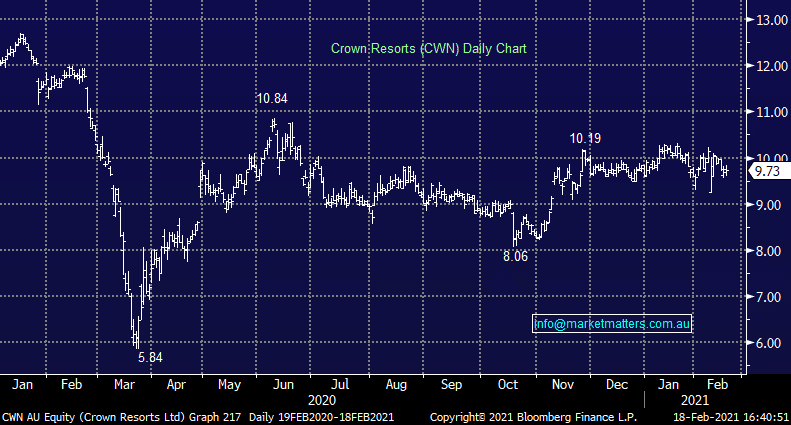

Crown (CWN) +0.41%: Not much point talking CWN earnings as they are largely irrelevant given the massive disruption in Melbourne and the big reform agenda now in front of them. These things (re-opening) plus board / management refresh will dictate the future of this iconic business. As it stands though, debt is the other major issue for them sitting at $1.2bn with around about 200m to spend on Crown in Sydney, however offsetting this is very strong apartment sales in Sydney (about $900m) with cheques starting to land. This will create a big de-gearing event throughout 2021 which is key, plus of coarse getting Sydney gaming operational and navigating other regulatory potholes in other states.

All in all, a lot going on for CWN however if they can get through it, their assets are worth a lot more than the market is giving them credit for. This is a higher risk position in the MM Growth Portfolio, however worth remembering that Wynn Resorts bid $14.75 per share in 2019 and Melco agreed to buy 20% at $13. There is value in them hills, the challenge is clearly unlocking it!

MM remains cautiously optimistic CWN

Add To Hit List