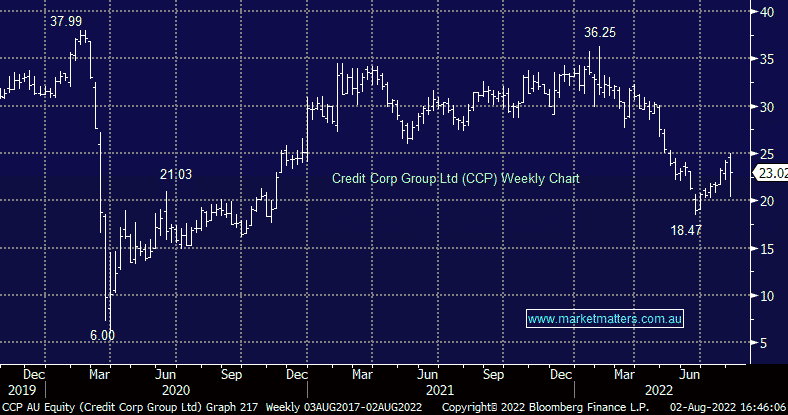

CCP -5.35%: The debt collector reported net income today of $100.7m for FY22, ahead of the $96.6m expected, and a final dividend of 36cps which was inline. The profit result equated to a 14% increase on FY21 so clearly a solid outcome, however, their guidance for FY23 caused some concern, they are guiding to net income of $90-$97m and Purchased Debt Ledger (PDL) acquisitions of $220-$260m. PDL’s are essentially their inventory, they buy the debts and then work to recover them, less availability of bad debts = less inventory = lower earnings. The stock was down ~15% in early trade but recovered throughout the session. On 14x FY23 earnings, CCP is about fair value in MM’s view.

MM is neutral/marginally positive CCP around $23.00

Add To Hit List