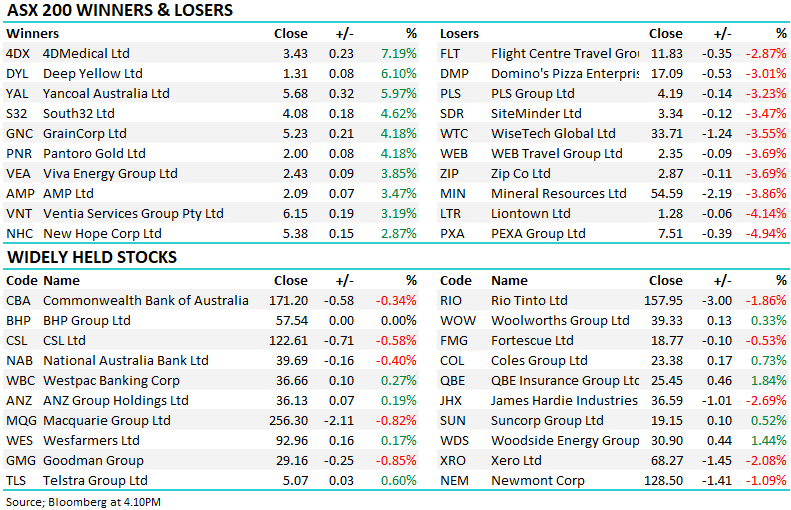

CAT +17.71%:Catapult was out with FY26 earnings this morning, and after speaking with management on the 9.30am call, we came away more positive on the result. The numbers were good on first pass, but the tone from management was also upbeat, particularly around the strength of the sales pipeline, the momentum in professional teams, and the opportunity to keep expanding the platform following the Perch and IMPECT acquisitions.

The market has clearly liked what it saw, with CAT shares up ~17% today, reversing some of the recent weakness in the stock. Revenue, Annualised Contract Value (ACV), Management EBITDA and free cash flow were all ahead of expectations, while the business continues to demonstrate the operating leverage we are looking for.

- Revenue increased 21% to US$140.7m, ahead of expectations for US$138.5m.

- Management EBITDA rose 67% to US$24.7m, beating expectations of US$20.3m and ahead of the company’s March guidance for ~50% growth.

- Annualised Contract Value (ACV) increased to US$133.8m, up 28% on a constant currency basis, or 18% excluding acquired ACV from Perch and IMPECT.

- SaaS revenue rose 21% to US$118.6m, while SaaS and other recurring revenue now represents 95% of total revenue.

- Free cash flow excluding transaction costs was US$6.5m, ahead of the March trading update range of US$5-6m.

- Catapult added 576 new Pro Teams during the year, while average ACV per Pro Team increased 10% to more than US$30,000.

- Retention remained above 96%, an important metric for a SaaS business.

- Rule of 40 reached a record 36% excluding acquired ACV, or 46% including acquired ACV, showing that growth and profitability are becoming better balanced.

Catapult is no longer just growing revenue; it is starting to convert that growth into earnings and cash flow. It is still early, and FY26 was clouded by acquisition activity, but the signs are increasingly clear that scale is flowing through the model. Management sounded confident that the business can keep growing ACV, maintain low churn, improve margins and generate higher free cash flow in FY27.

ACV remains the key metric to watch. It is Catapult’s lead indicator of future revenue, and 28% growth was strong. Importantly, even excluding acquired ACV from Perch and IMPECT, ACV still grew 18%, suggesting the core business is continuing to expand rather than relying solely on M&A.

The professional team metrics were particularly encouraging. Catapult added 576 new Pro Teams, grew average ACV per team by 10%, and maintained retention above 96%. That is a strong combination: the company is landing new customers, expanding existing relationships, and maintaining stickiness. The surge in multi-vertical pro-team customers was outstanding, which supports the view that the broader platform strategy is working.

The acquisitions of Perch and IMPECT are important in this context. Catapult is moving beyond athlete tracking and video analysis into a more integrated sports performance, coaching, gym monitoring and scouting intelligence platform. Tactics & Coaching ACV grew strongly, with the Ord’s Analyst Amelia Hamer noting 43% growth in the vertical, suggesting IMPECT is performing well. The more workflows CAT can own inside a professional sports organisation, the more valuable and embedded the platform becomes. That also helps reduce the threat from AI, because CAT’s competitive advantage increasingly comes from proprietary data, workflow integration and deep customer relationships.

Guidance remains qualitative rather than specific, which is typical for Catapult. Management said it expects strong ACV growth, low churn, continued margin improvement and higher free cash flow in FY27. The balance sheet is also in good shape, with more than US$53m of cash and no debt, giving the company flexibility to keep investing in the platform while maintaining financial discipline.

Overall, this was a strong result, and the management call reinforced our positive view. The share price reaction today reflects relief after recent weakness, but also growing confidence that CAT is scaling in the right direction. The stock still has plenty more room to recover.

MM is long & bullish CAT in the Emerging Companies Portfolio

Add To Hit List