The Bunnings landlord has been on the radar for the Emerging Companies Portfolio since January when we took a closer look at their takeover of retail landlord Newmark Property (NPR) covered here. Ultimately, we have held off adding BWP to the portfolio, preferring to hold Centuria Capital (CNI) for property exposure while the deal played out. NPR shares were suspended yesterday on compulsory acquisition grounds, given more than 90% of shares were now controlled by BWP. The scrip offer effectively brought in Newmark’s portfolio at a ~20% discount to NTA with a read-through cap rate of ~6%. Given that BWP was trading on a single-digit discount to NTA and a cap rate closer to 5.5%, this deal was accretive for shareholders, i.e. issuing relatively expensive scrip for cheaper assets.

- The key word here is “relatively.” We don’t view BWP as expensive, it still trades on a discount to NTA and a cap rate nearer to 5.5% is reasonable given the quality portfolio they run with conservative gearing and long-term leases. With the bulk of new shares already issued to NPR shareholders, the stock is likely past much of the potential acquisition selling.

The transaction does change the focus of the company, switching from an asset base that is 95%+ leased to Bunnings, now adding 9 large format retail assets with tenants including Wesfarmers (includes Bunnings, Kmart & Officeworks) and JB Hi-Fi. Still, ~80% of the portfolio is leased to high-quality, ASX200 listed tenants on long-term leases with a Weighted Average Lease Expiry (WALE) of ~5.5 years. The key to this deal creating value for shareholders will be, i) reducing gearing and cost of debt, & ii) continuing to execute on the quality assets with rental growth.

- We like the deal and are backing BWP to execute from here.

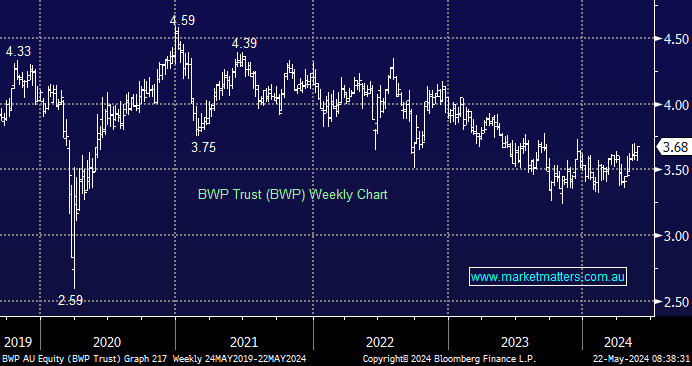

MM is bullish BWP

Add To Hit List